Summary

Key tasks performed

Skip to design

The context

What is Limitly?

Who is it for?

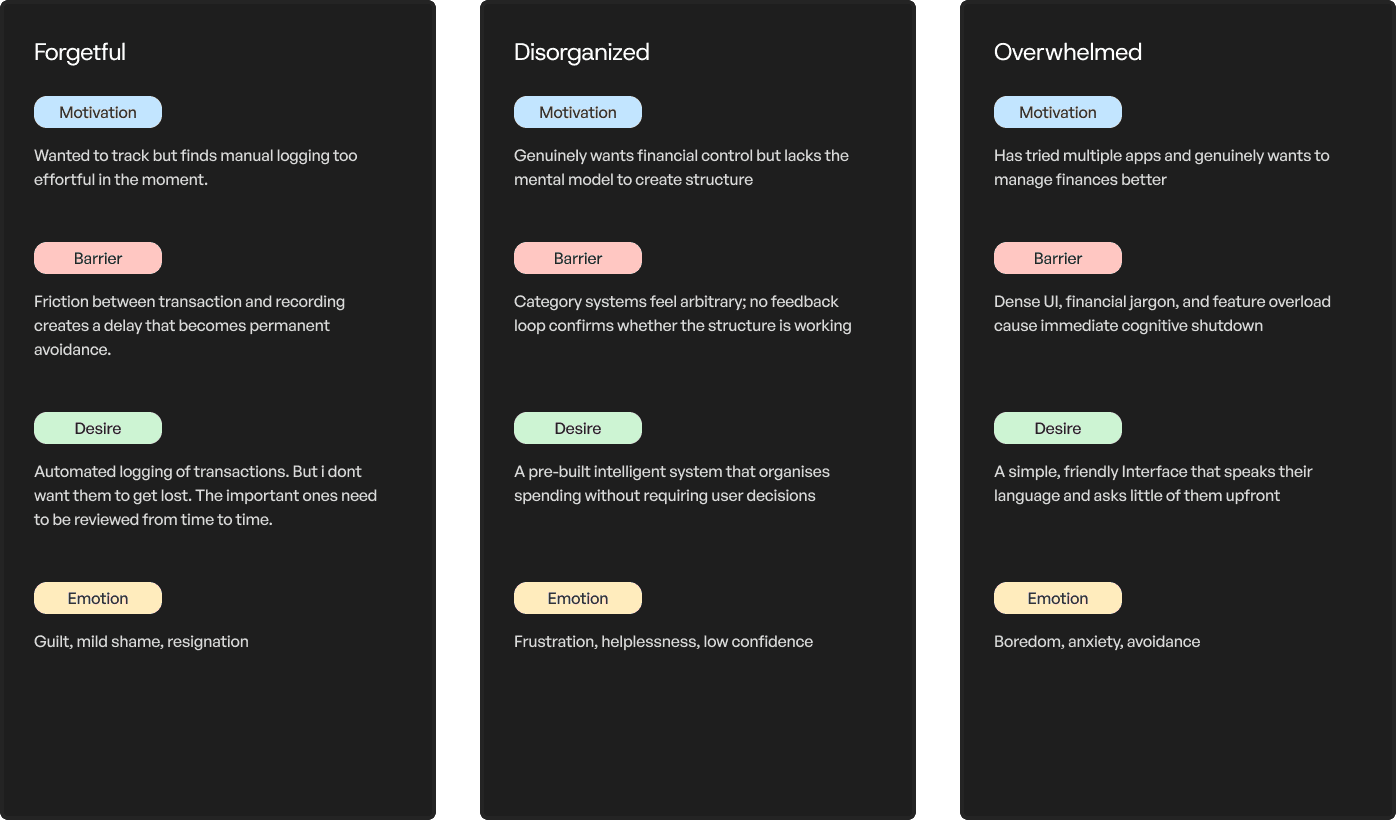

Students (18-24)

Students building money habits

Learning to budget save, and grow

Early Professionals

Starting careers & managing income

Building financial stability & savings

Self-Employed/Buisness owners

Managing multiple or project based income

Tracking multiple cash flows & staying in control

So, whats the problem?

1

Value proposition not instantly clear

2

High cognitive load in early onboarding

3

Insights lack clear priority

4

Trust is asked for but remains unexplained

Audience

Stated friction

Core JTBD blockers

Alright, time for some research

What are the people saying?

Identifying proof from secondary sources to validate the problems people were facing

Emotions in the background

Retention reality

46%

of Gen Z feel confident about managing their own finances

CoinLaw, 2025

73%

abandon apps during onboarding due to design problems alone

SaaS Factor, 2024

68%

of Gen Z identify money stress as their top mental health concern

Bank of America, 2024

39%

would delete a finance app after a single security issue

EY, cited in Contentworks, 2024

10–15%

Day 7 retention rate — regardless of motivation in all sectors

ContextSDK, 2024

Okay, lets try and fix that

Before designing a solution it was worth understanding what had already been tried and where there was genuine room to improve.

Cleo

Users: 8M+ users (2025)

Market: United States only

Audience: Gen Z, paycheck-to-paycheck workers, (18–30)

Cleo proved that tone is a product decision, not a copywriting one. By replacing clinical financial language with a conversational, occasionally irreverent voice, Cleo made a category that typically triggers anxiety feel approachable — even on a bad spending day. Users did not feel judged. They felt talked to.

Fold

Users: 600K+ (Nasdaq-listed FLD, 2025)

Market: -

Audience: Crypto-curious spenders, (20–35), BTC enthusiasts

Fold proved that structure is the product. By building automatic expense categorisation from day one, users never had to organise anything themselves — the system existed before they arrived. Fold showed that the biggest drop-off trigger isn't complexity. It's the blank page. Give people a starting point, and they stay.

Revolut India

Users: 50M+ globally, 40M+ active (2025)

Market: UK, EU, US, expanding APAC

Audience: 25–40, frequent travellers, multi-currency

Revolut proved that the moment of spending is the moment to intervene. Instant notifications and smart budgeting tools meant users never had to manually log a thing. The app already knew. Revolut showed that frictionless financial visibility is a baseline, not a premium. Awareness without effort is the real product.

Curie money UPI

Users: ~1L downloads, beta until Oct 2025

Market: India only (Bengaluru-based)

Audience: Salaried Indians seeking yield on idle cash

Curie Money proved that your money should work even when you don't. By parking balances in liquid mutual funds with a 6.7% interest annually, while keeping them ready for instant UPI payments. Users changed nothing about their behaviour. Passive growth is the retention hook.

Feature comparison matrix

Limitly vs all 4 competitors across their feature listings

Not Available

Implemented

Partially Implemented / Similar Approach

Opportunity areas

Show value before asking for anything

Replace enforcement with understanding

Make money grow while it sits

Turn money management into a challenge

Okay now how do we go about implementing this?

01

Using research findings to inform design

02

Test and validate design decisions

03

Refine & iterate

Alright, lets Design

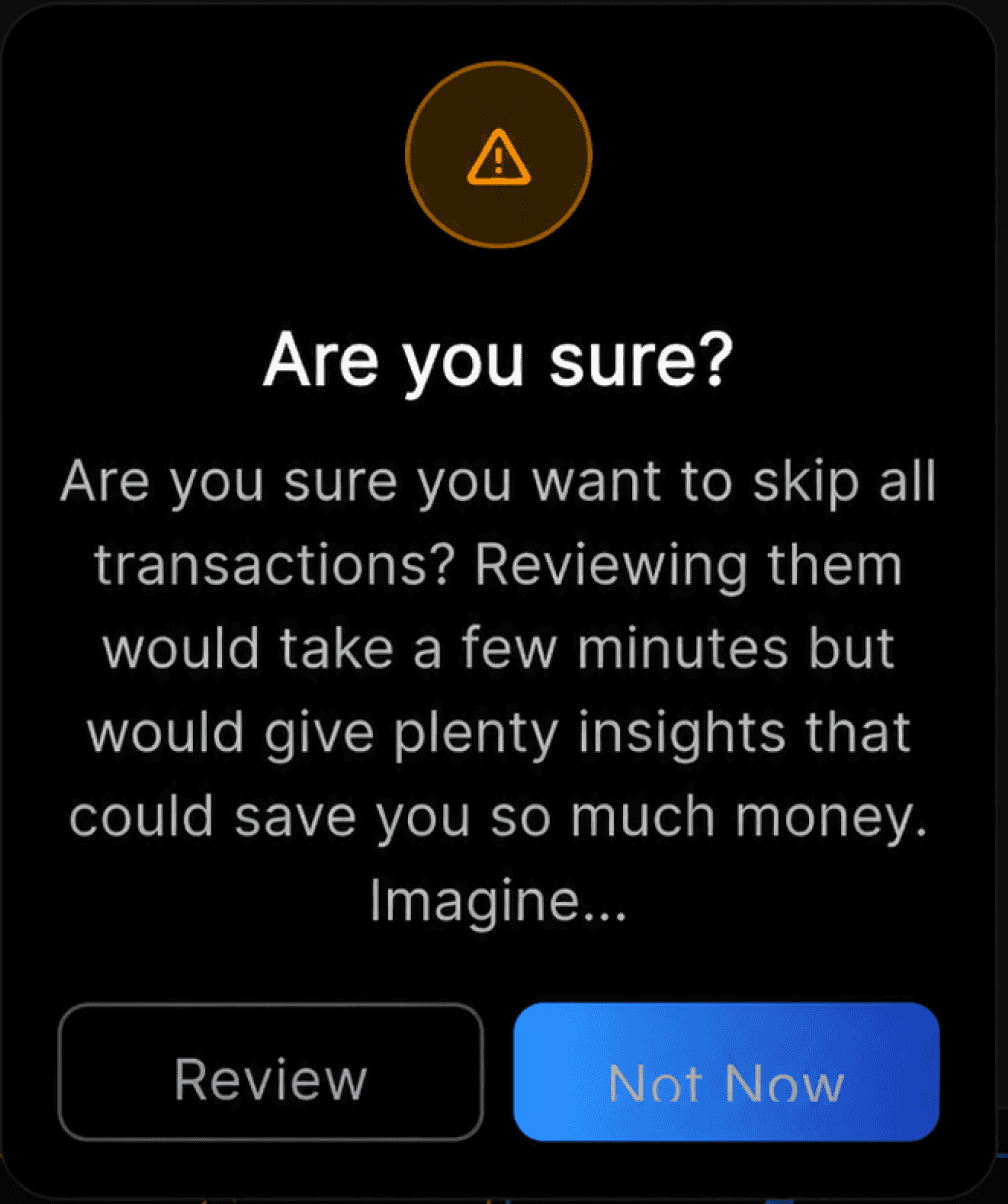

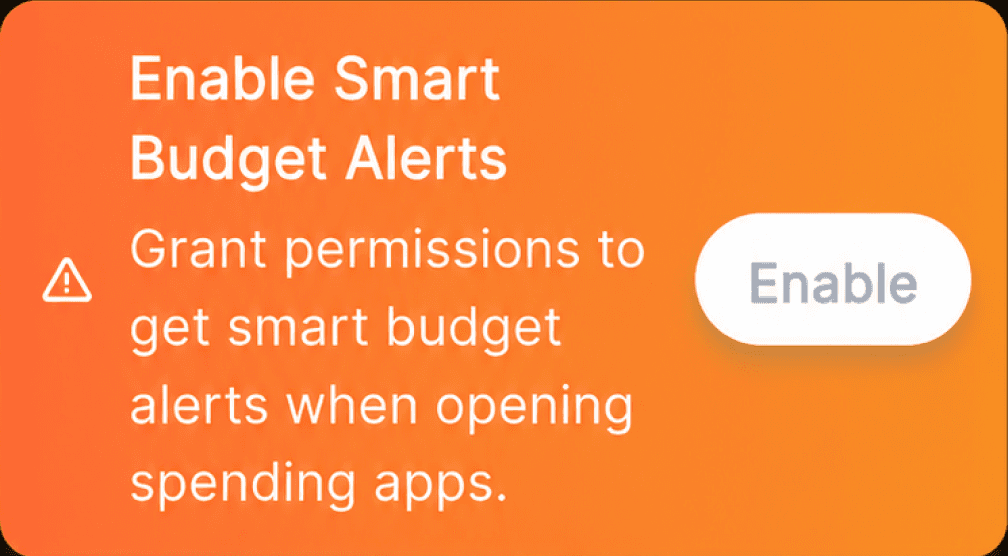

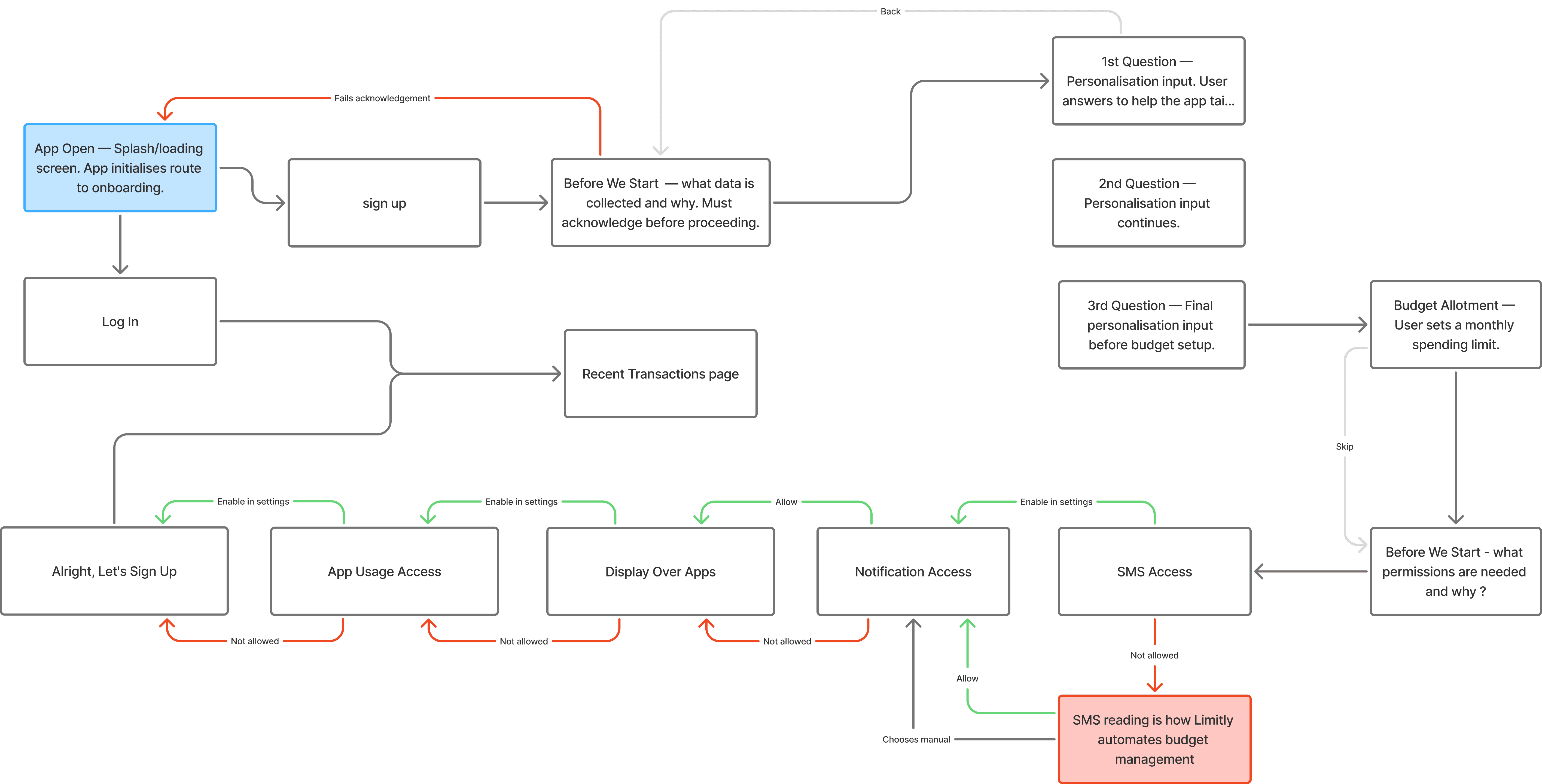

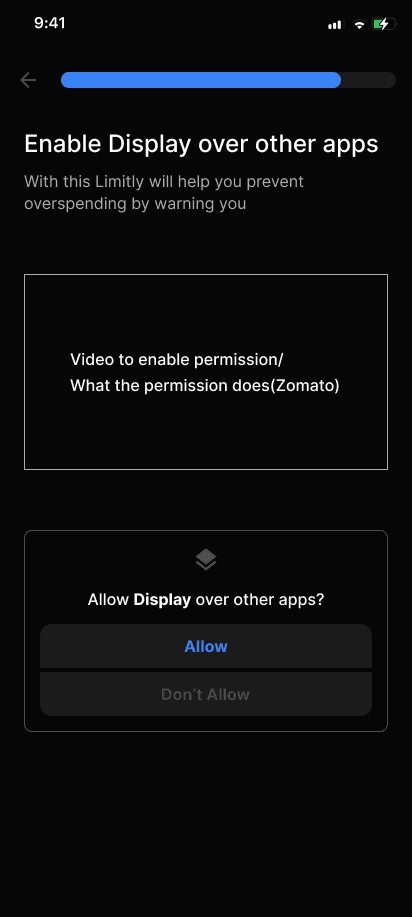

One of the biggest challenges was the onboarding flow, becuase there wasn't one to begin with

Inititially users were pushed to:

sign up—give permissions—review transactions—home screen

before they understood what the features are and how they were

adding value.

Trust is a scary thing in Fintech, you can't be pushy.

Speed was key.

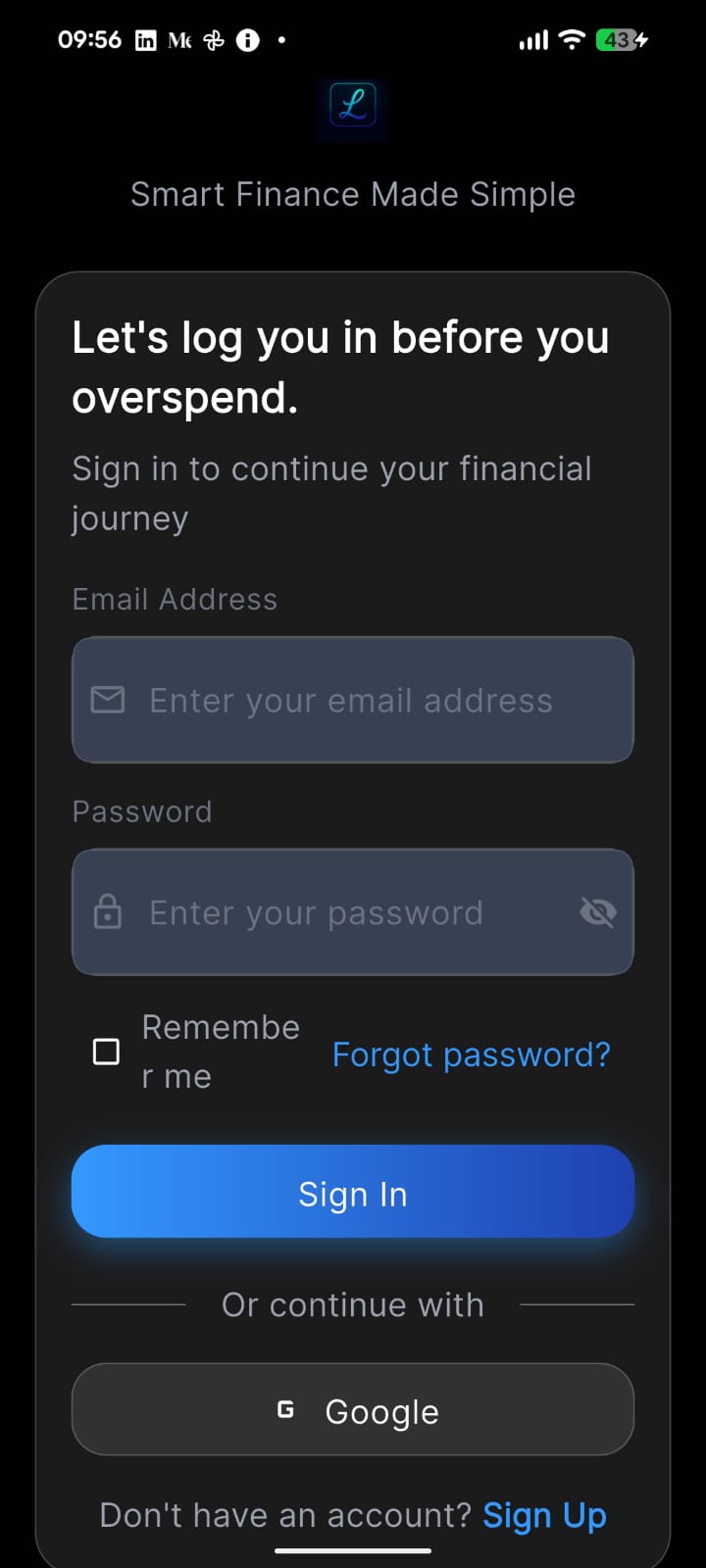

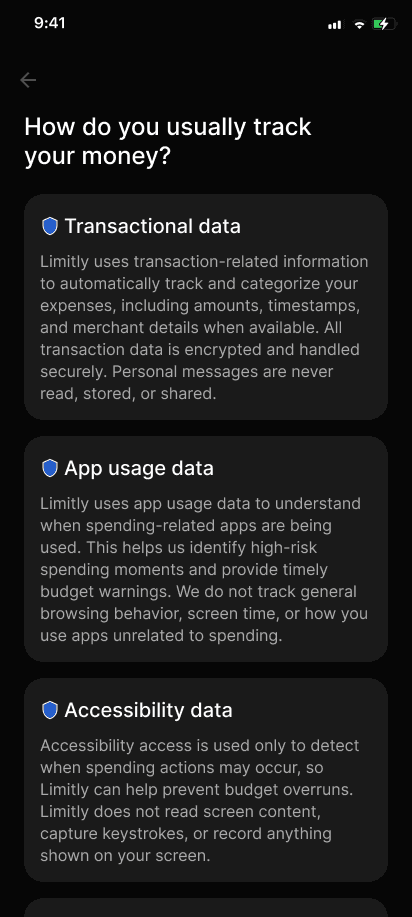

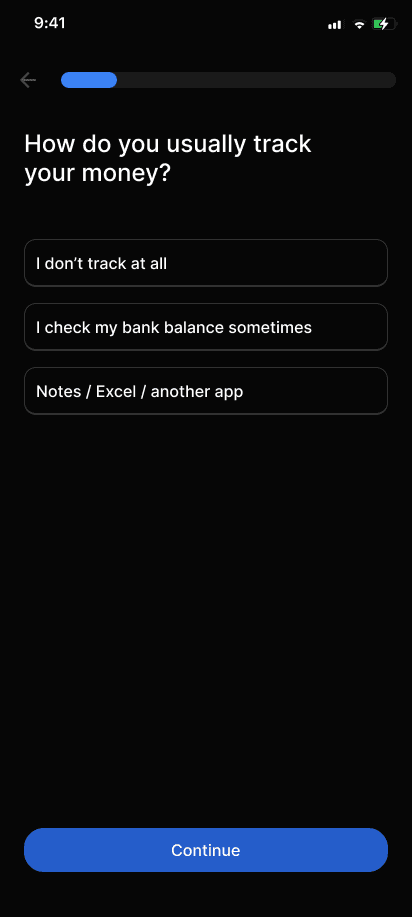

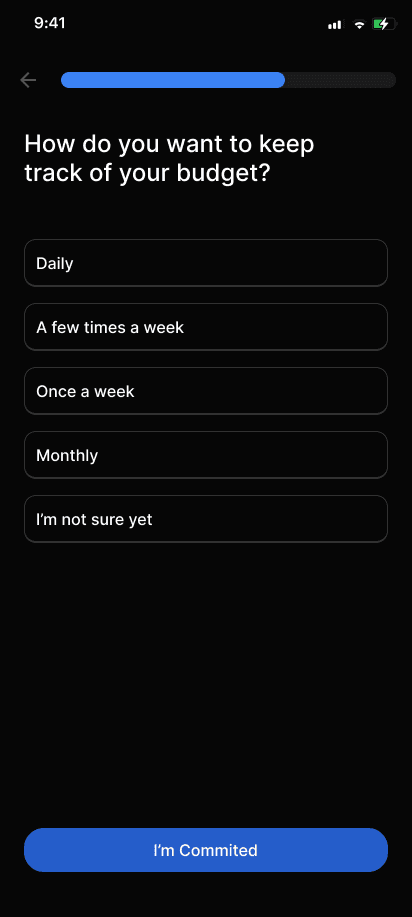

Using Claude we built a complete onboarding experience, focusing on clearer Value Propositions and personalization to build trust at early stages.

Onboarding user flow

Wireframes / Mid-fidelity screens

The first sprint

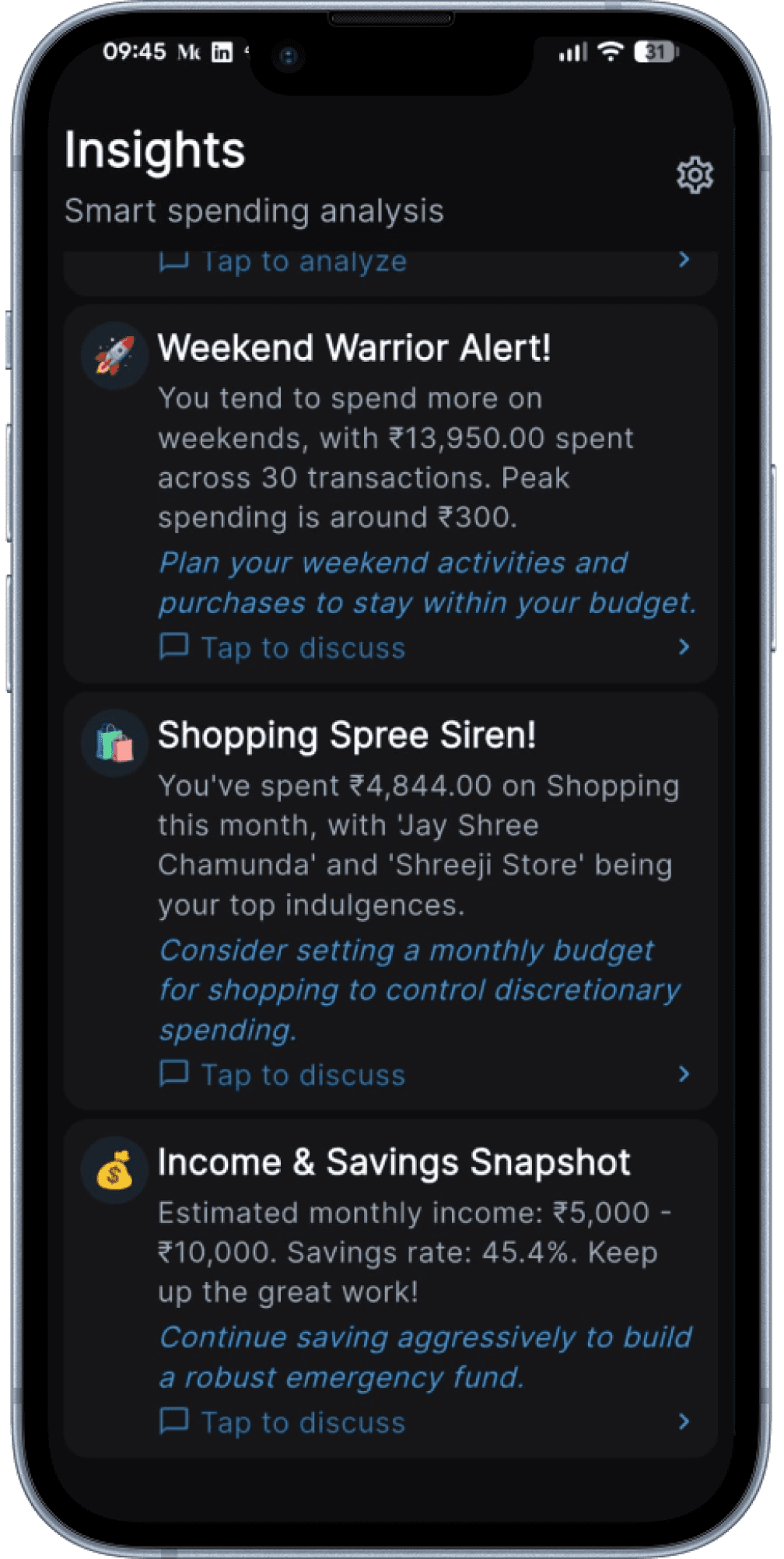

We then proceeded to update the landing pages for each of the following sections/features in the application.

since the budget page did most of the heavy lifting we decided to scrap the idea of having a home section.

As for insights page which was filled with paragraphs worth of warnings or actionable insights, felt too overwhelming and it was easy to miss out on important stuff.

Other Key screens

Great, now lets test it

Results of user testing

Most users were dropping off due to bug reports in the application, but that is expected at the initial stages.

However, it created an opportunity for the design team to address deeper product challenges related to the application’s information architecture and user journeys.

Lets Refine and Iterate

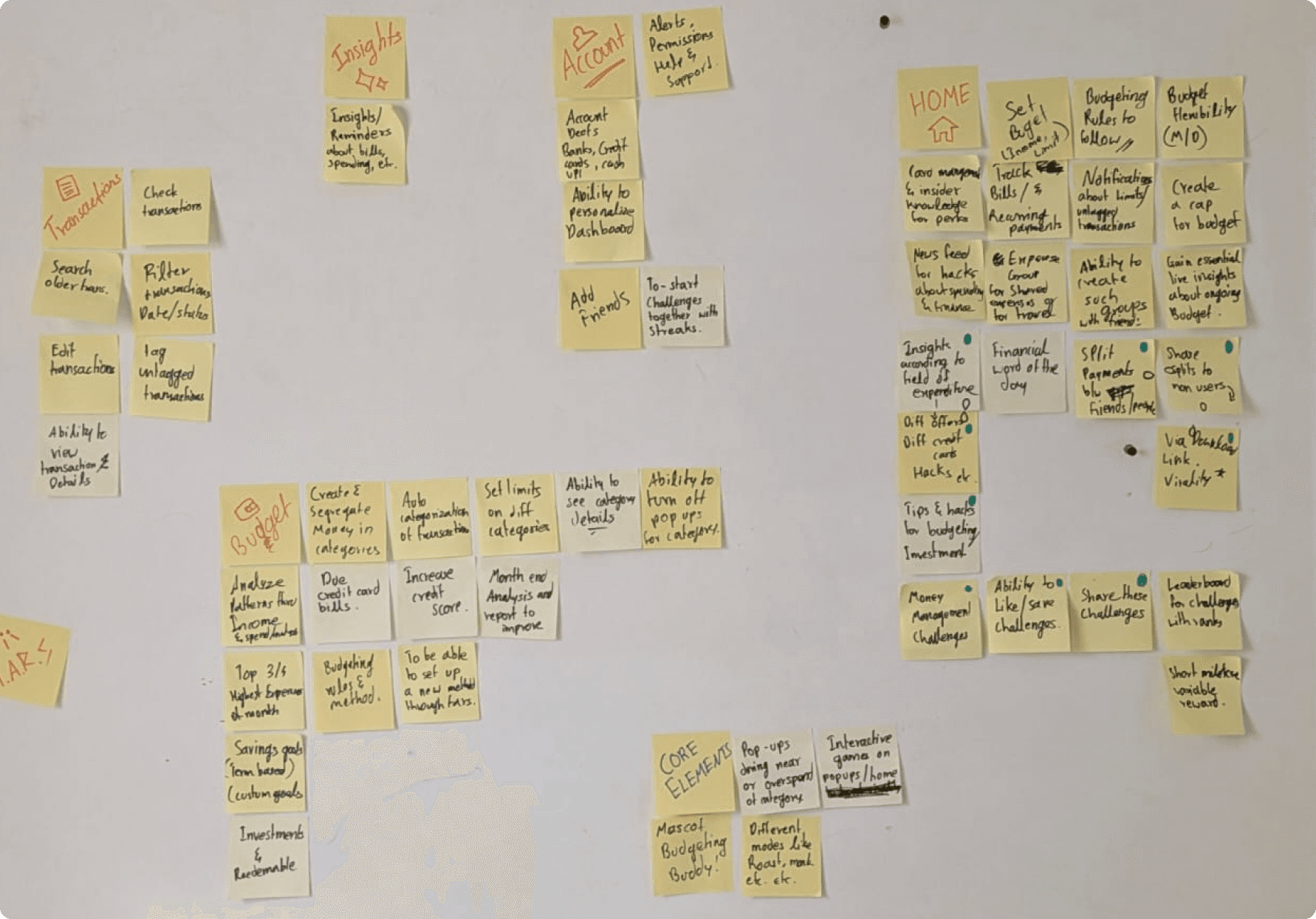

Card Sorting

This helped map limitly's overlapping features into distinct, navigable sections. This allowed users to find what they needed without friction.

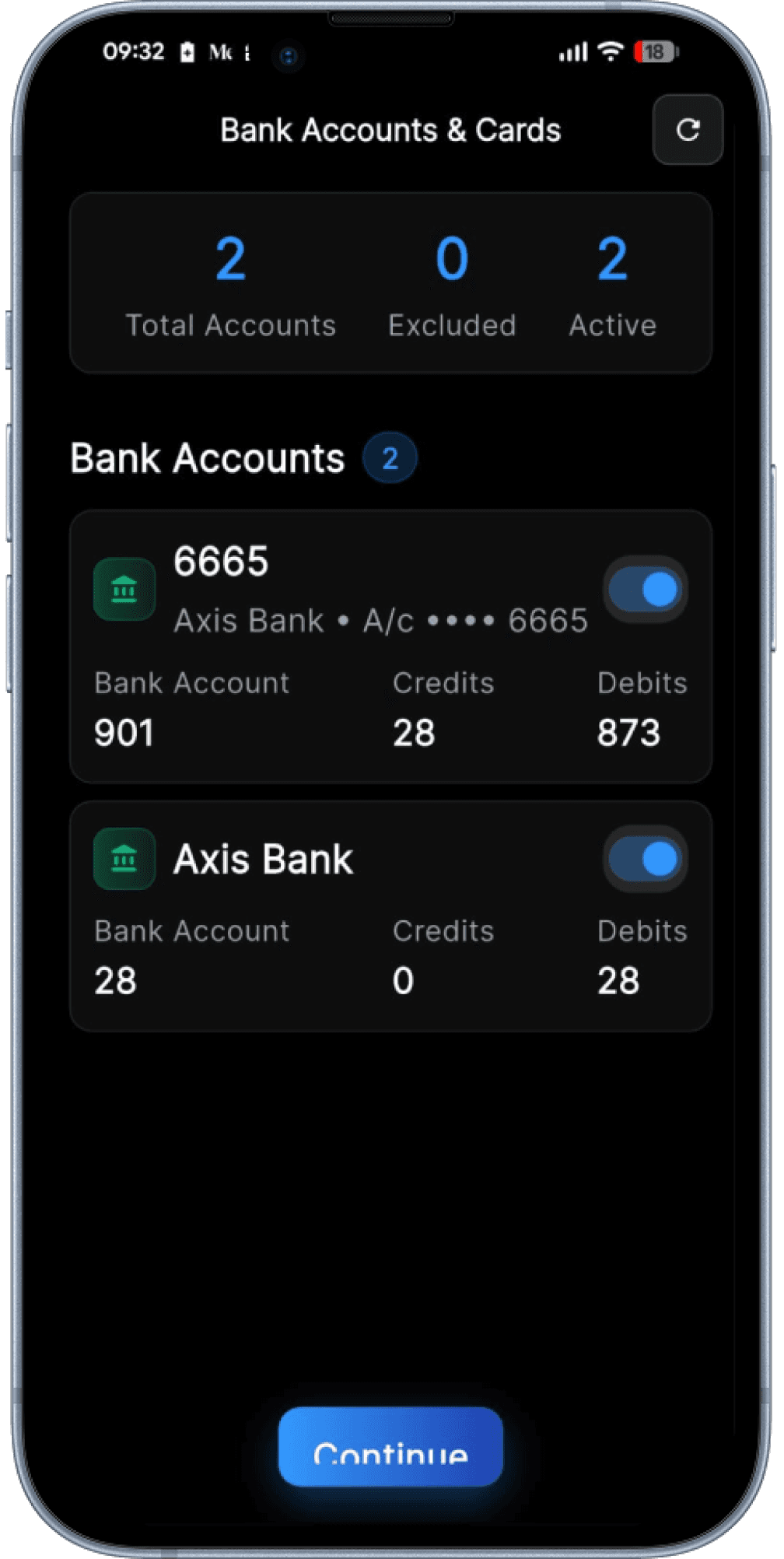

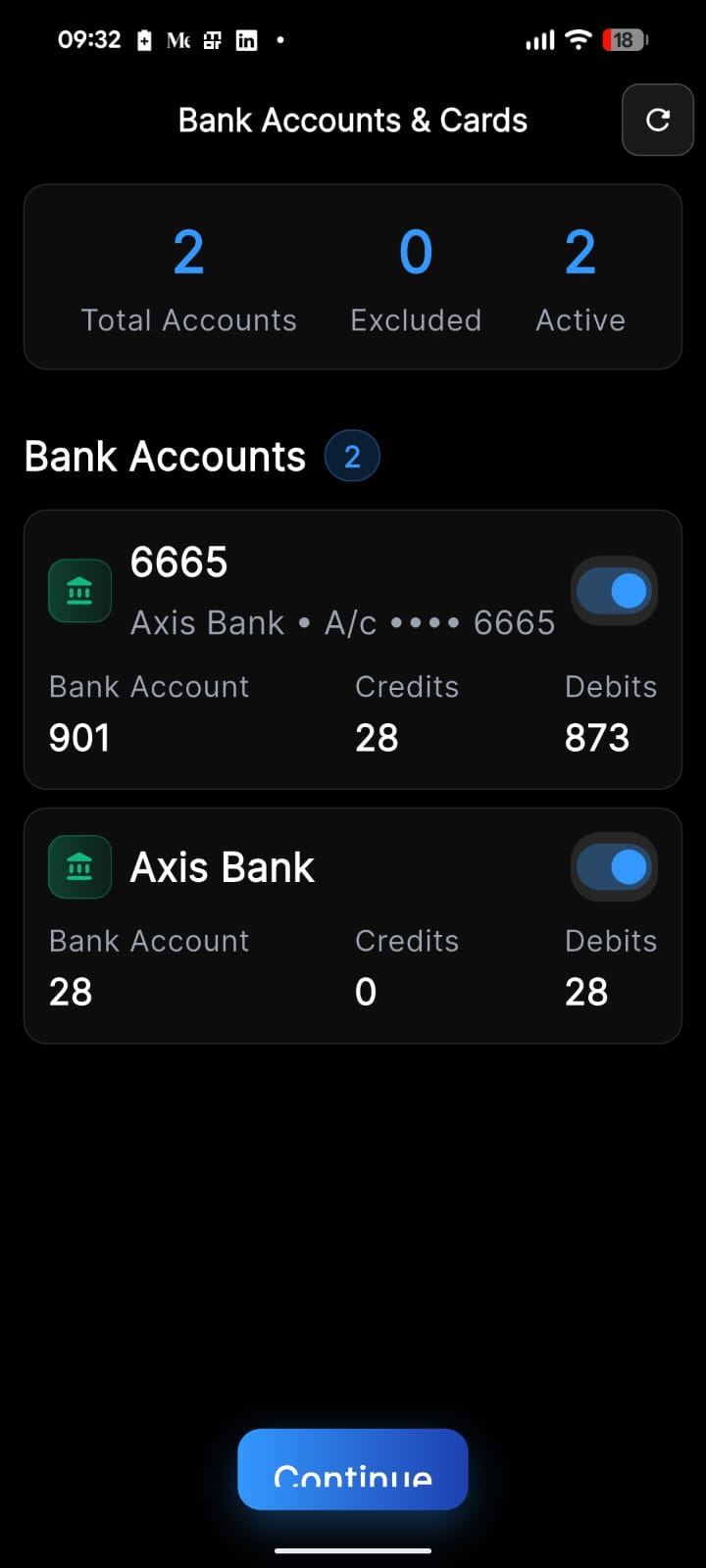

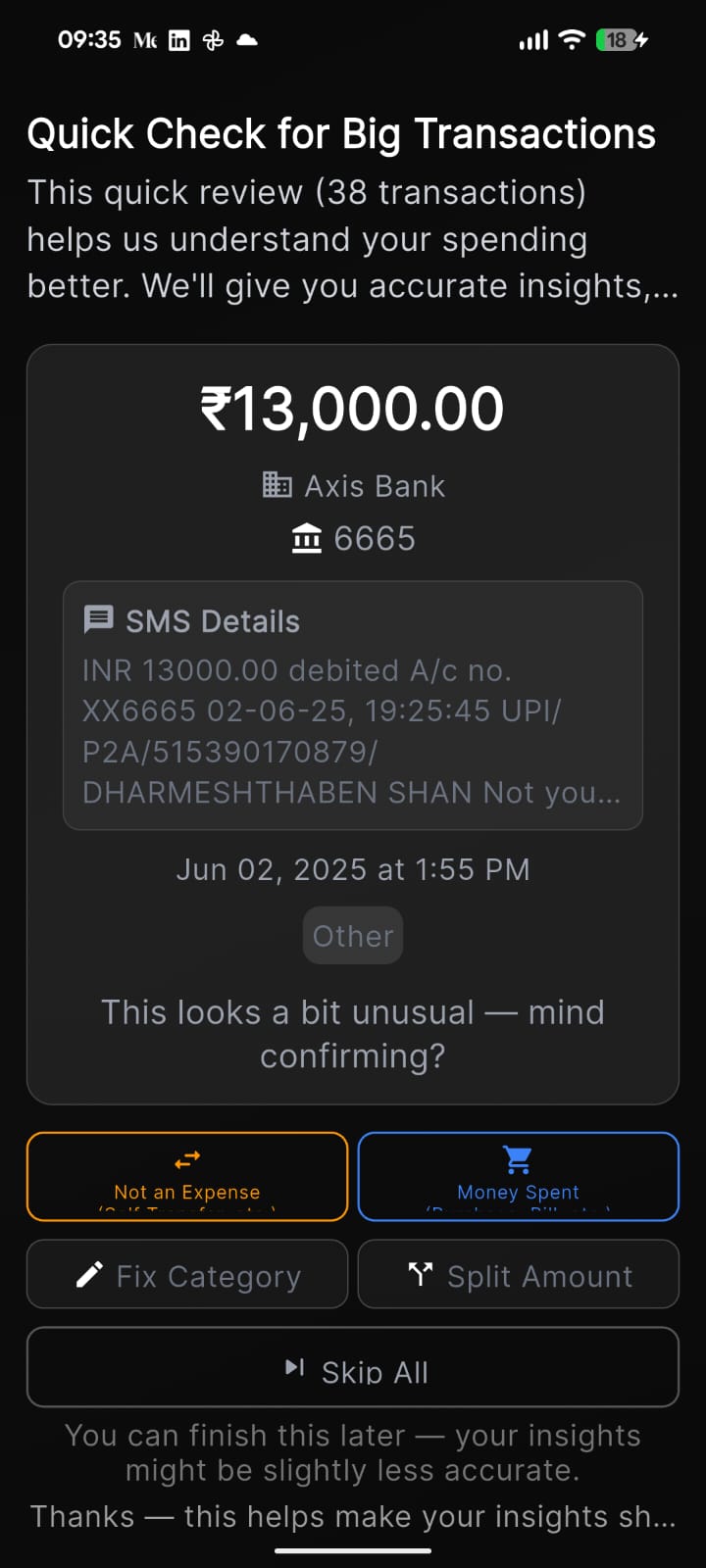

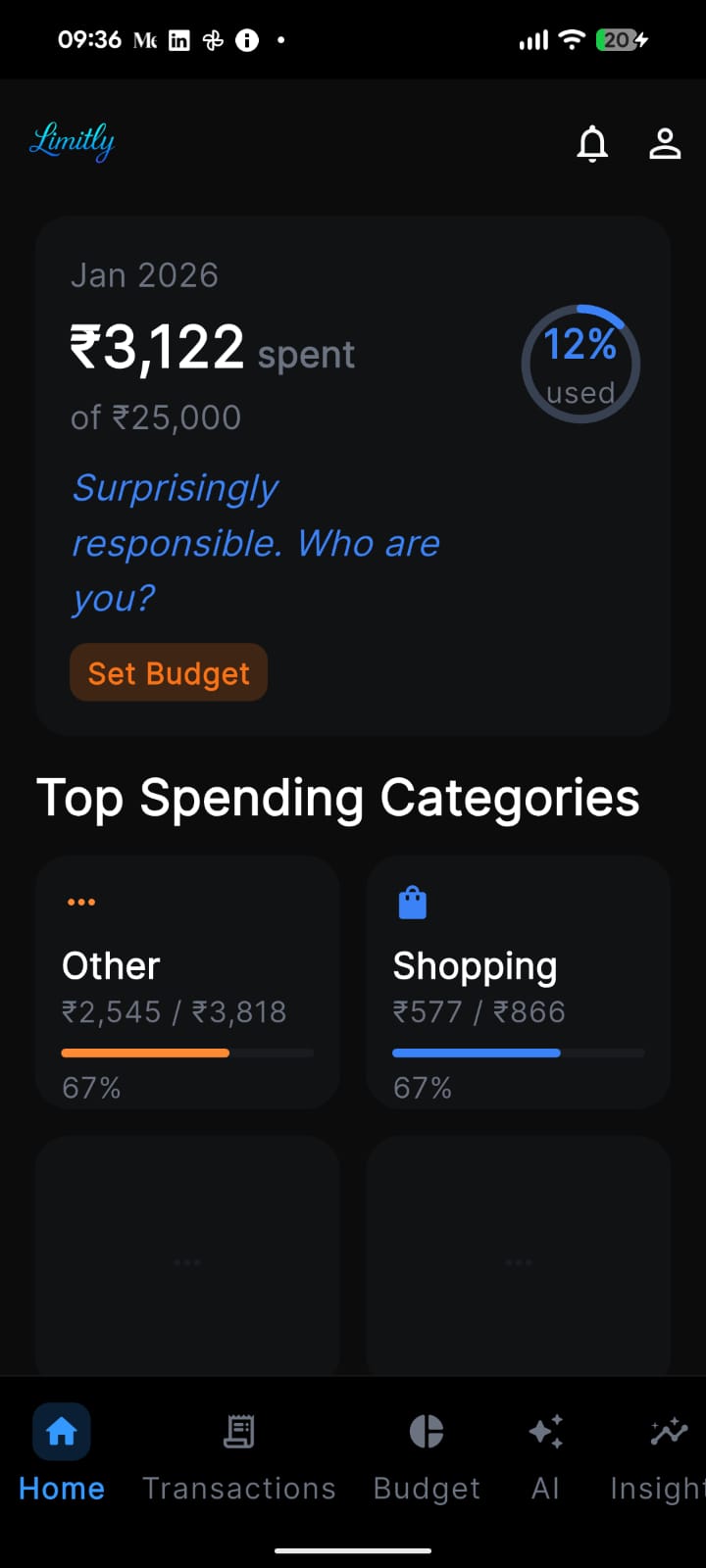

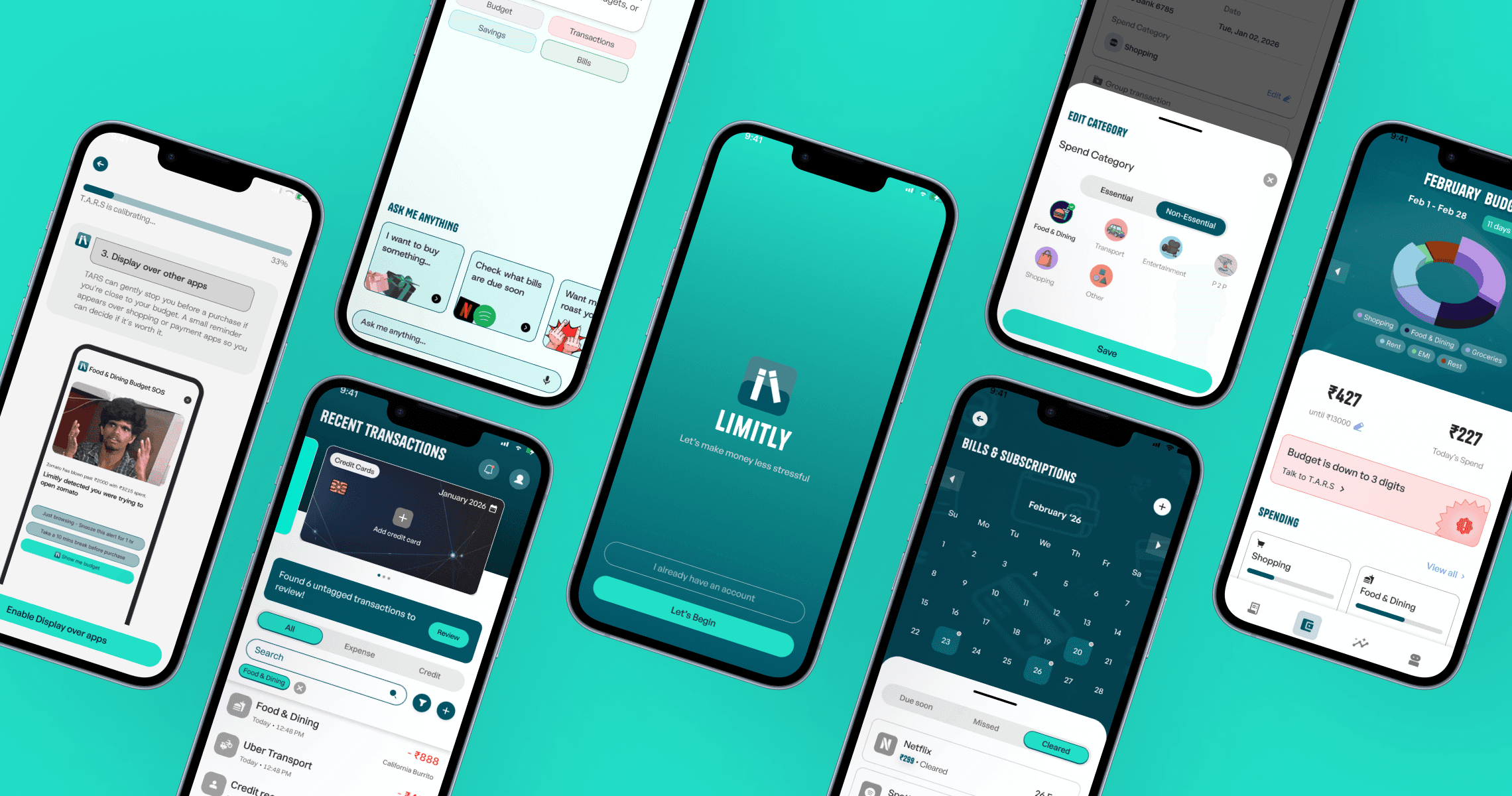

Final Designs

Onboarding

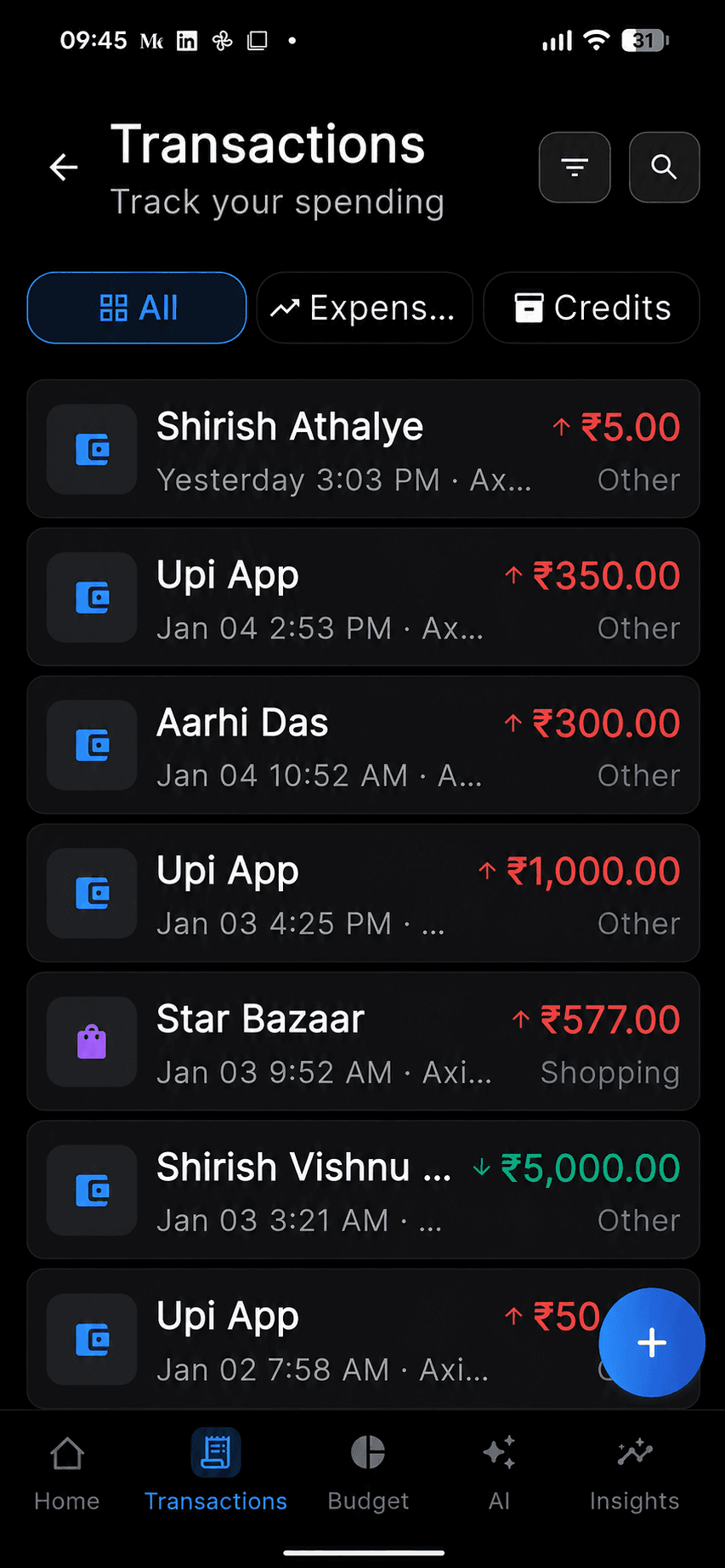

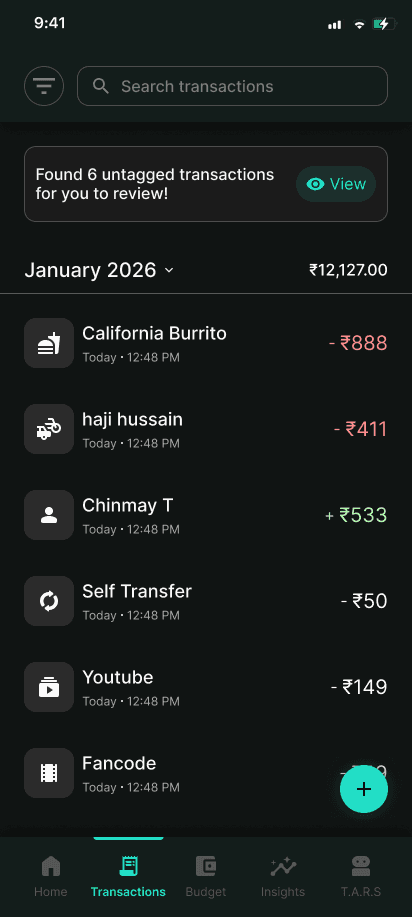

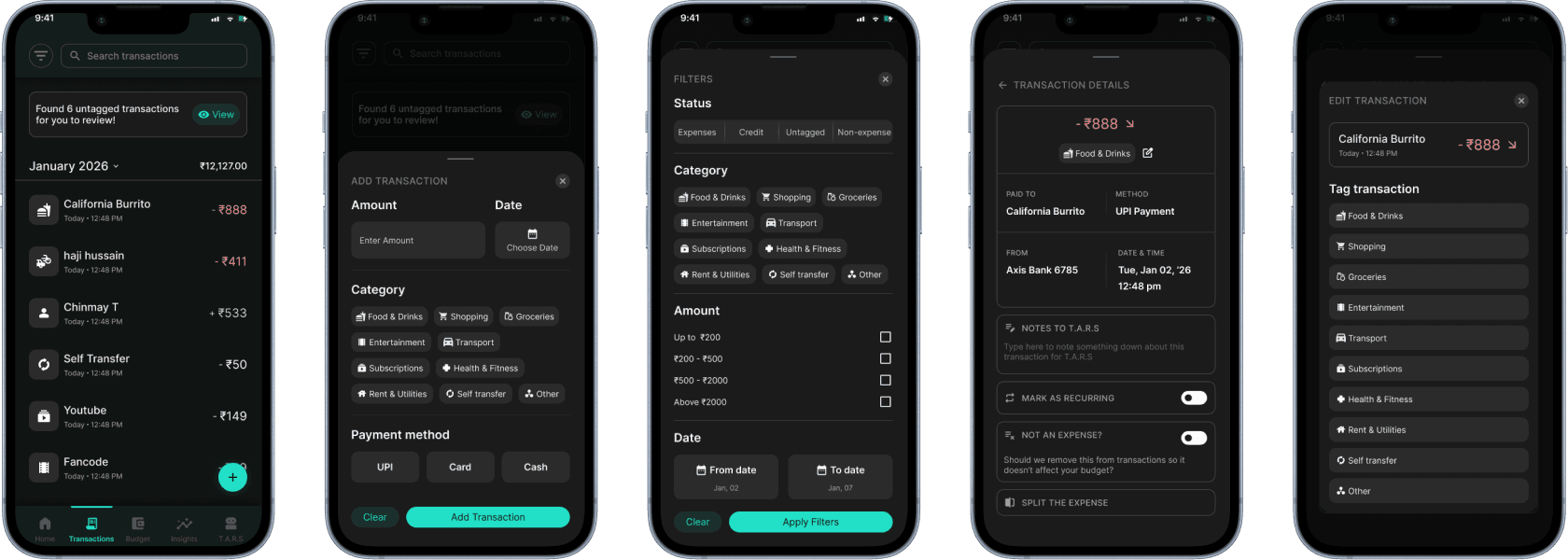

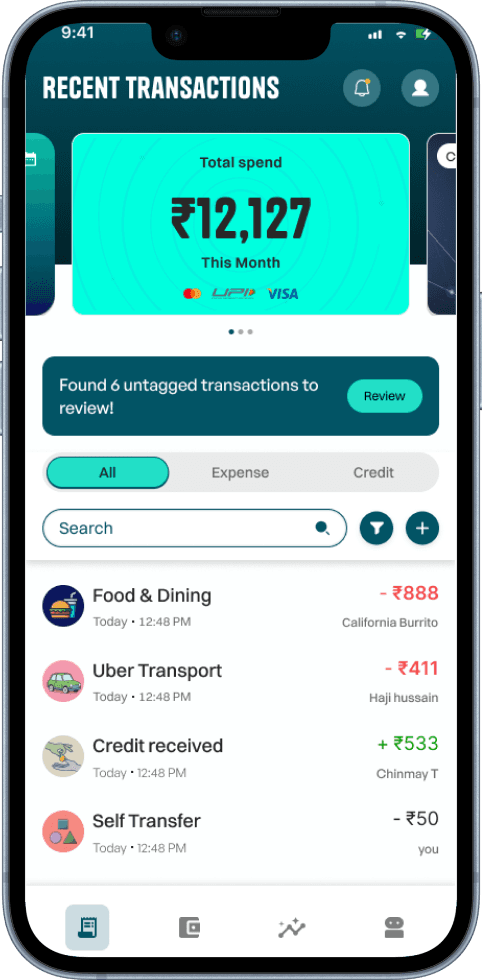

Recent transactions

Transaction review

Adding transaction

Transactions page

Recent transactions

Transaction review

Adding transaction

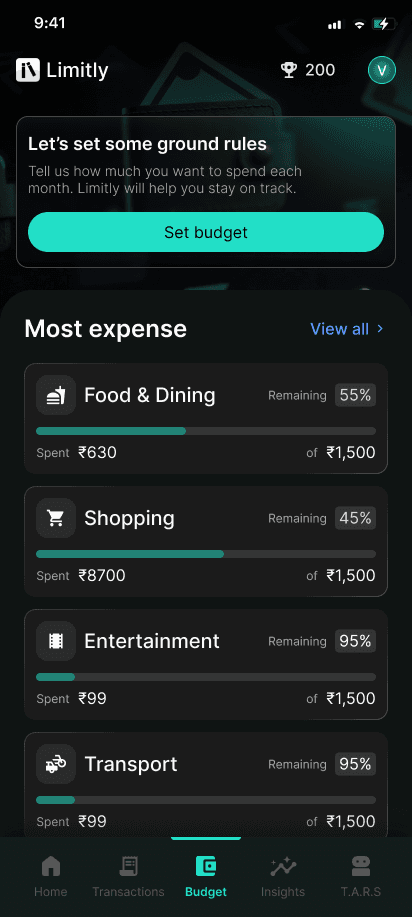

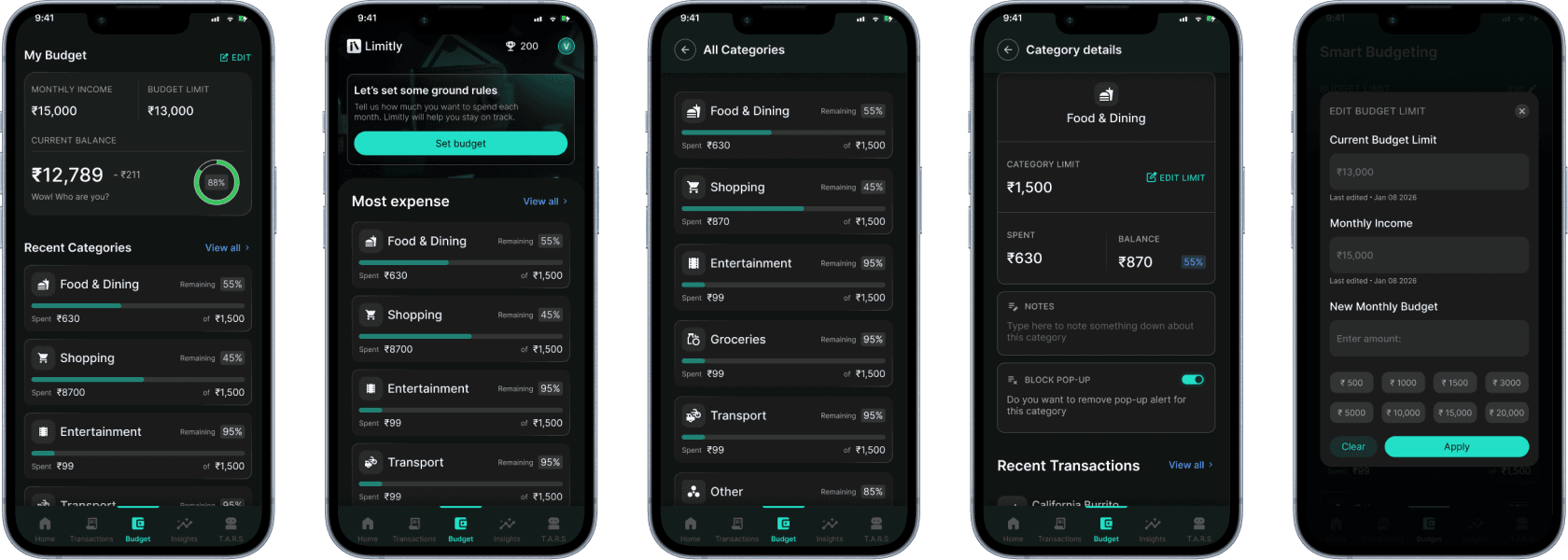

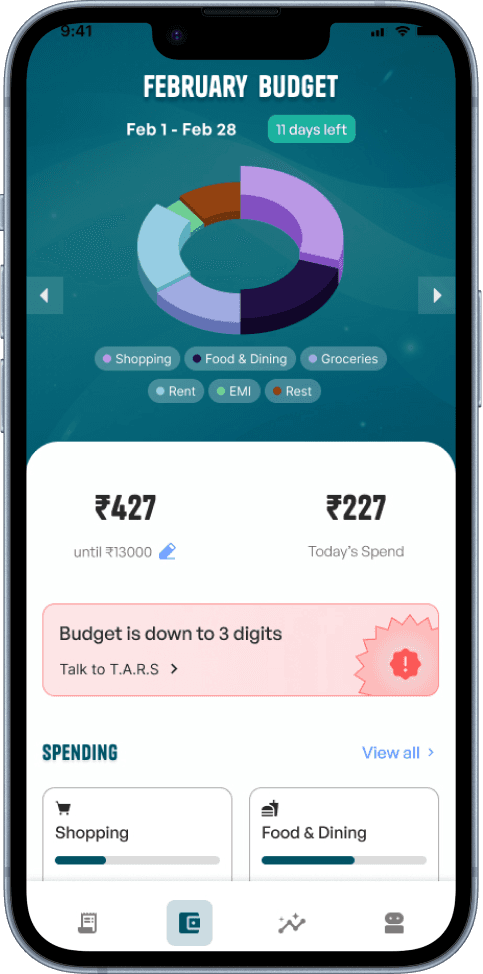

Budget page

Monthly budget

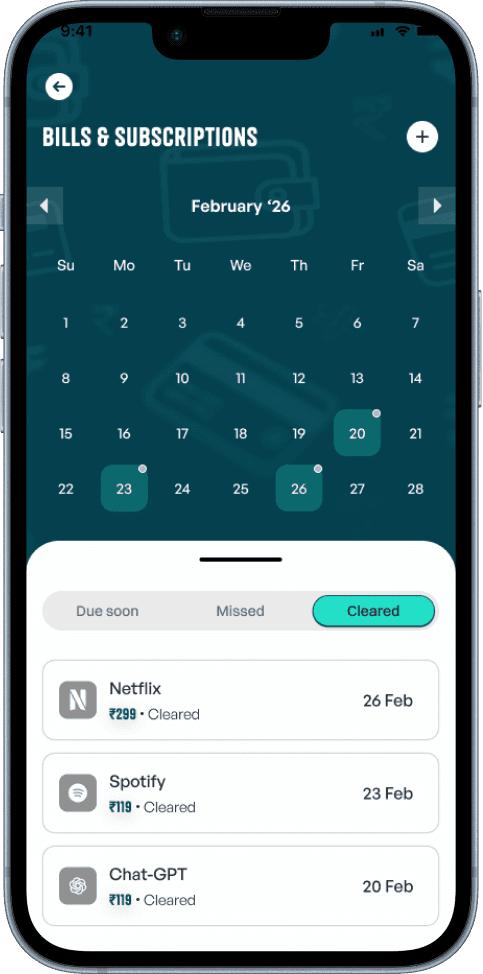

Bills & subscriptions

Spending categories

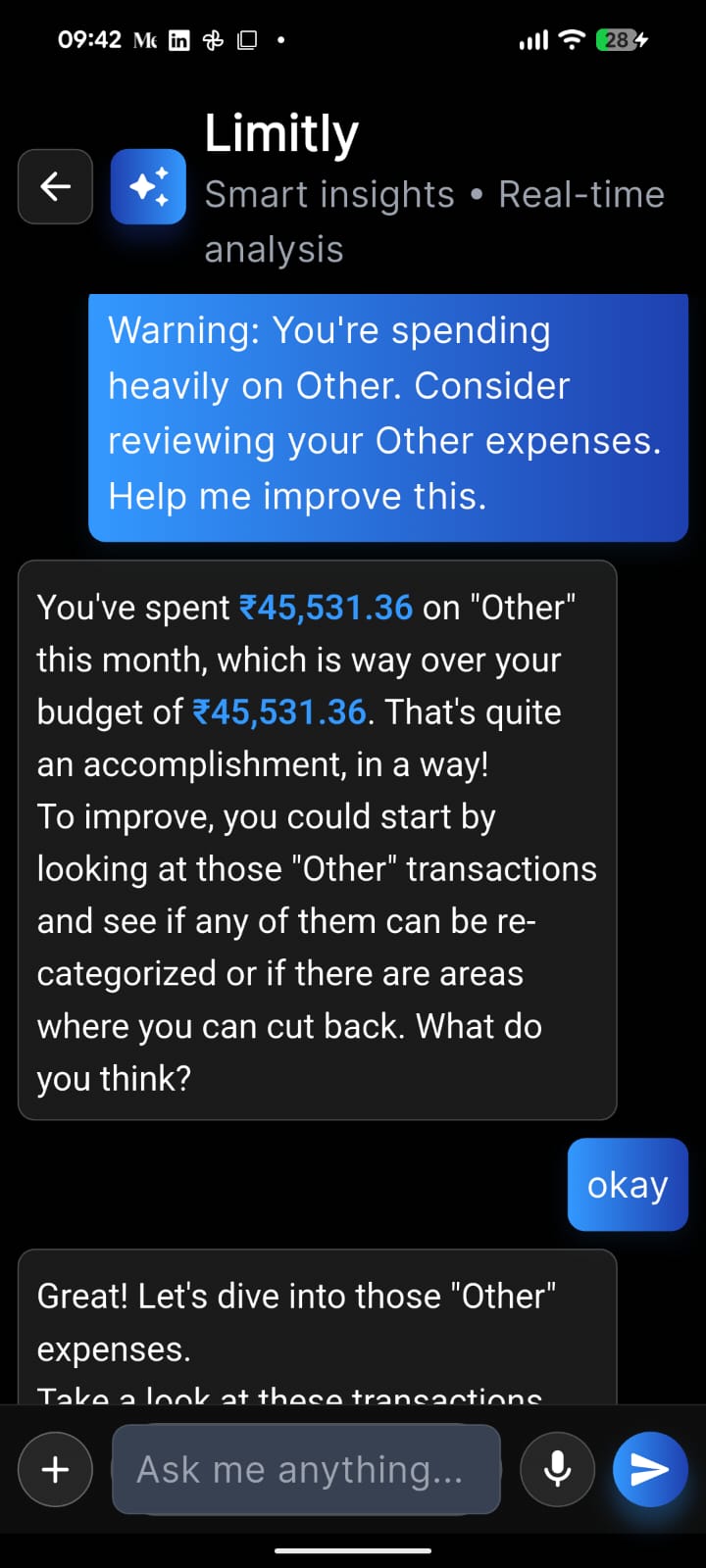

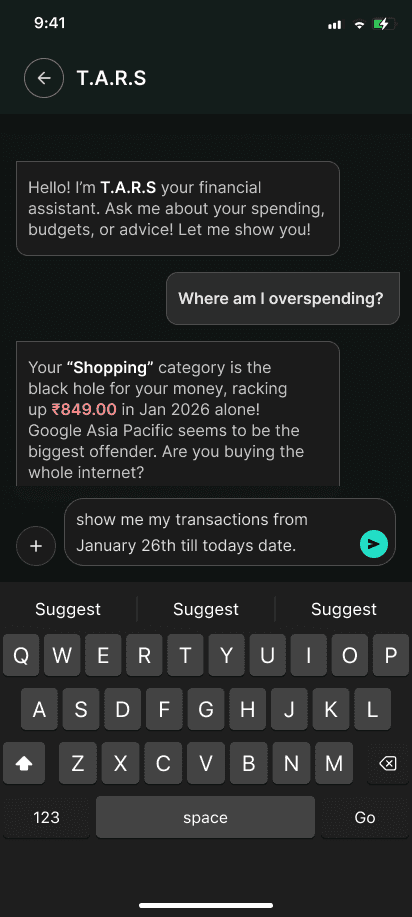

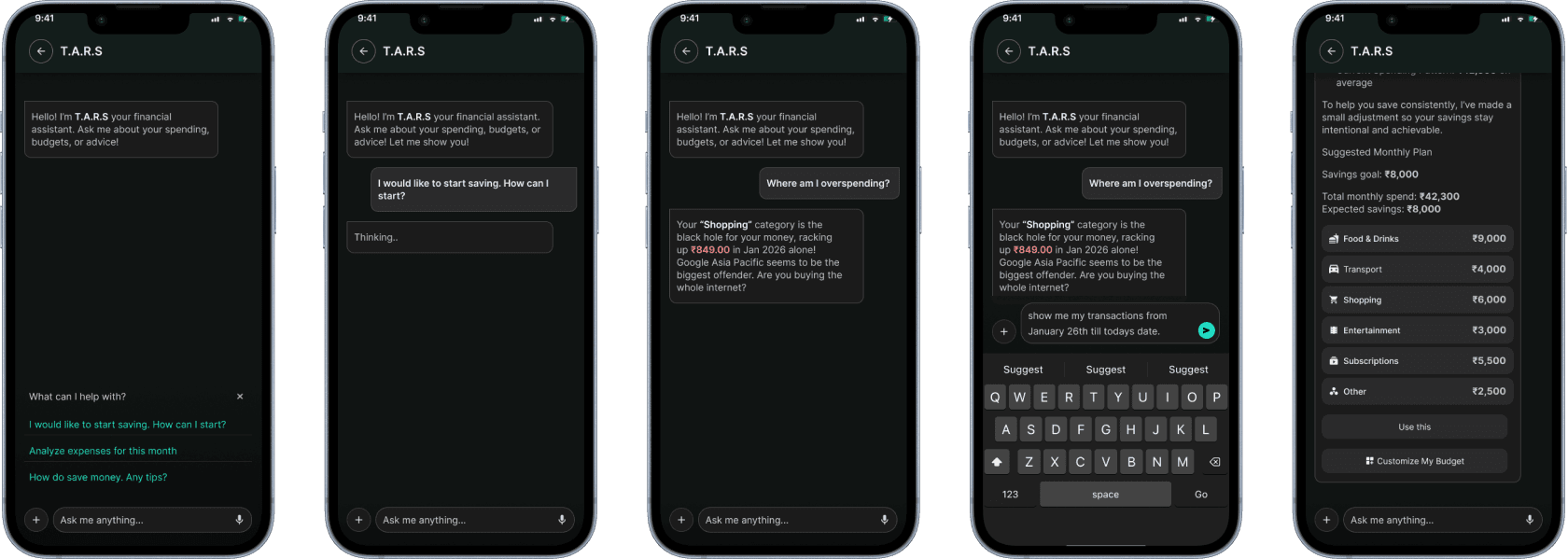

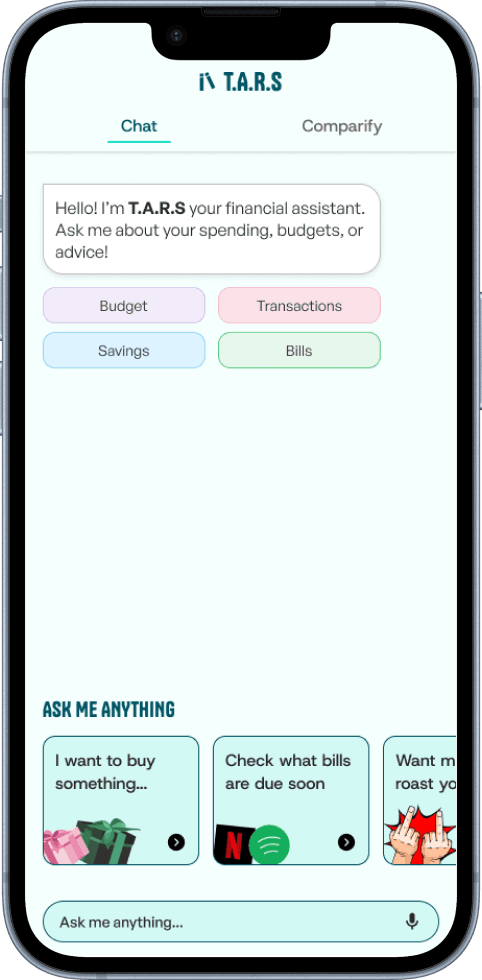

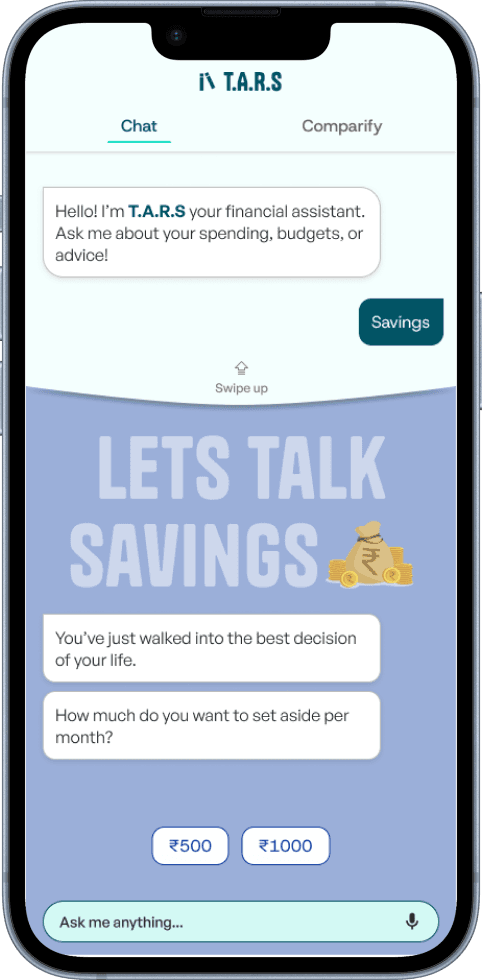

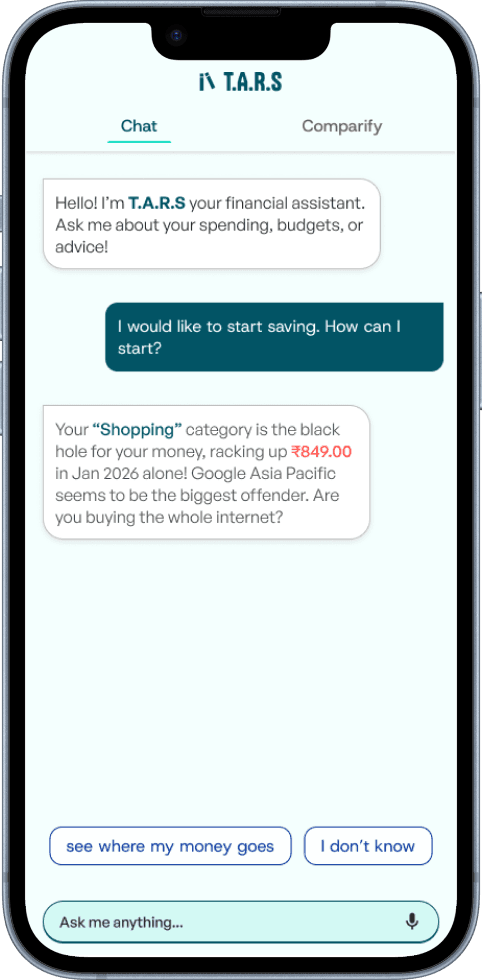

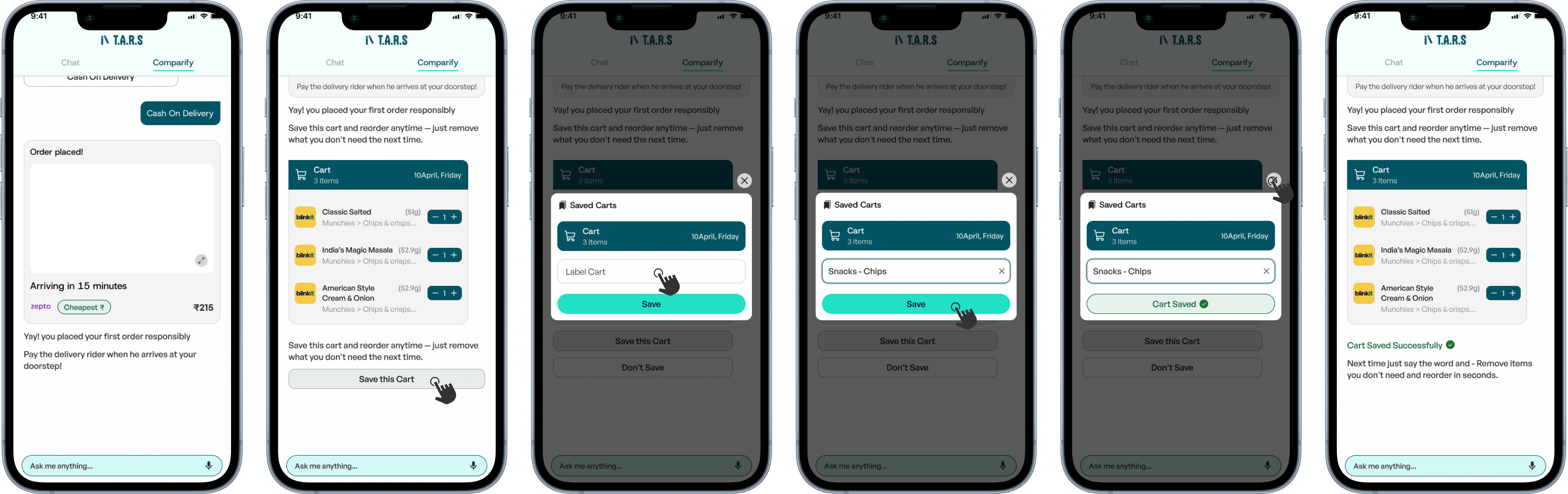

T.A.R.S

T.A.R.S

Savings section

How T.A.R.S replies

Cool, so what's next?

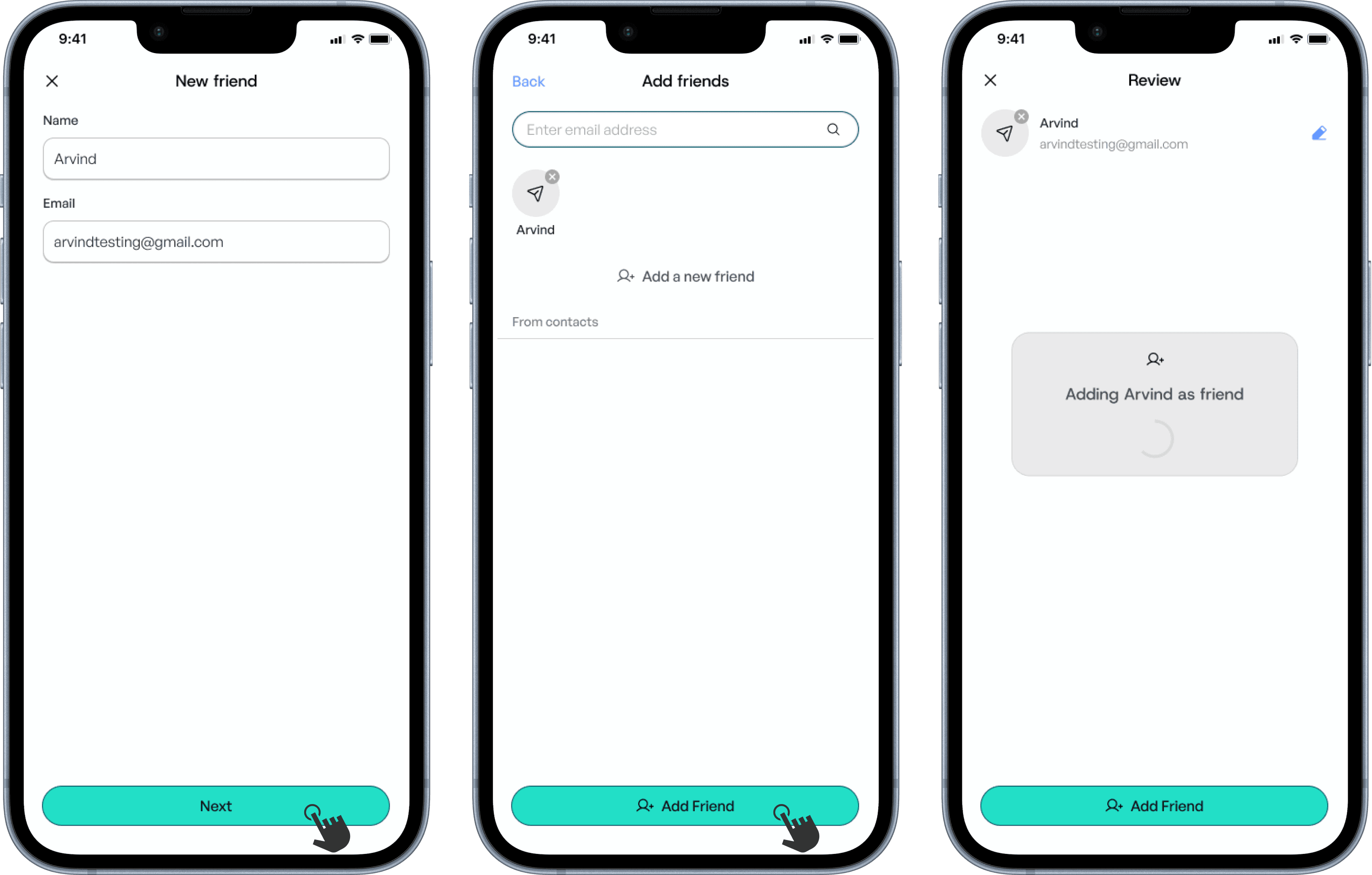

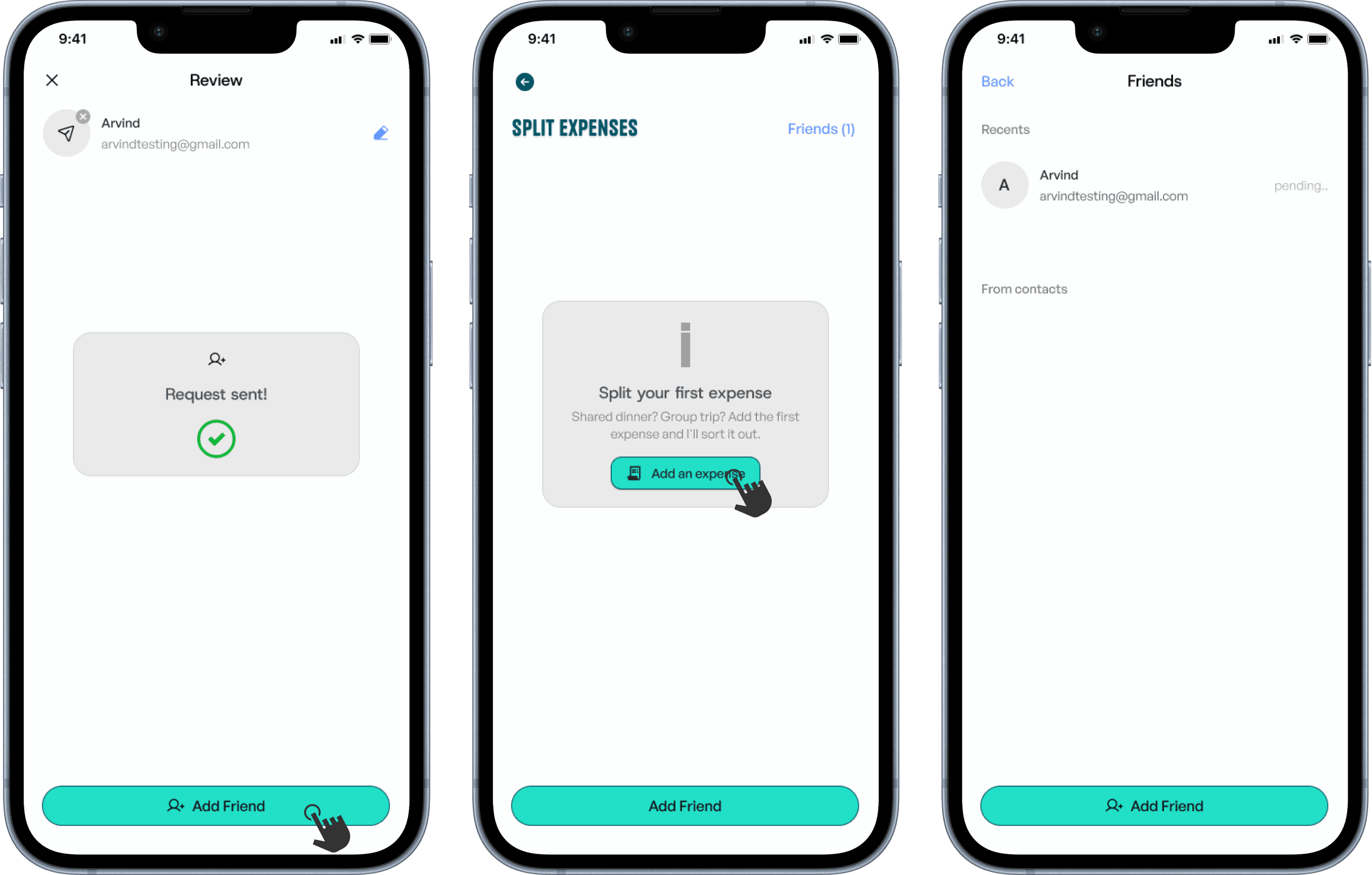

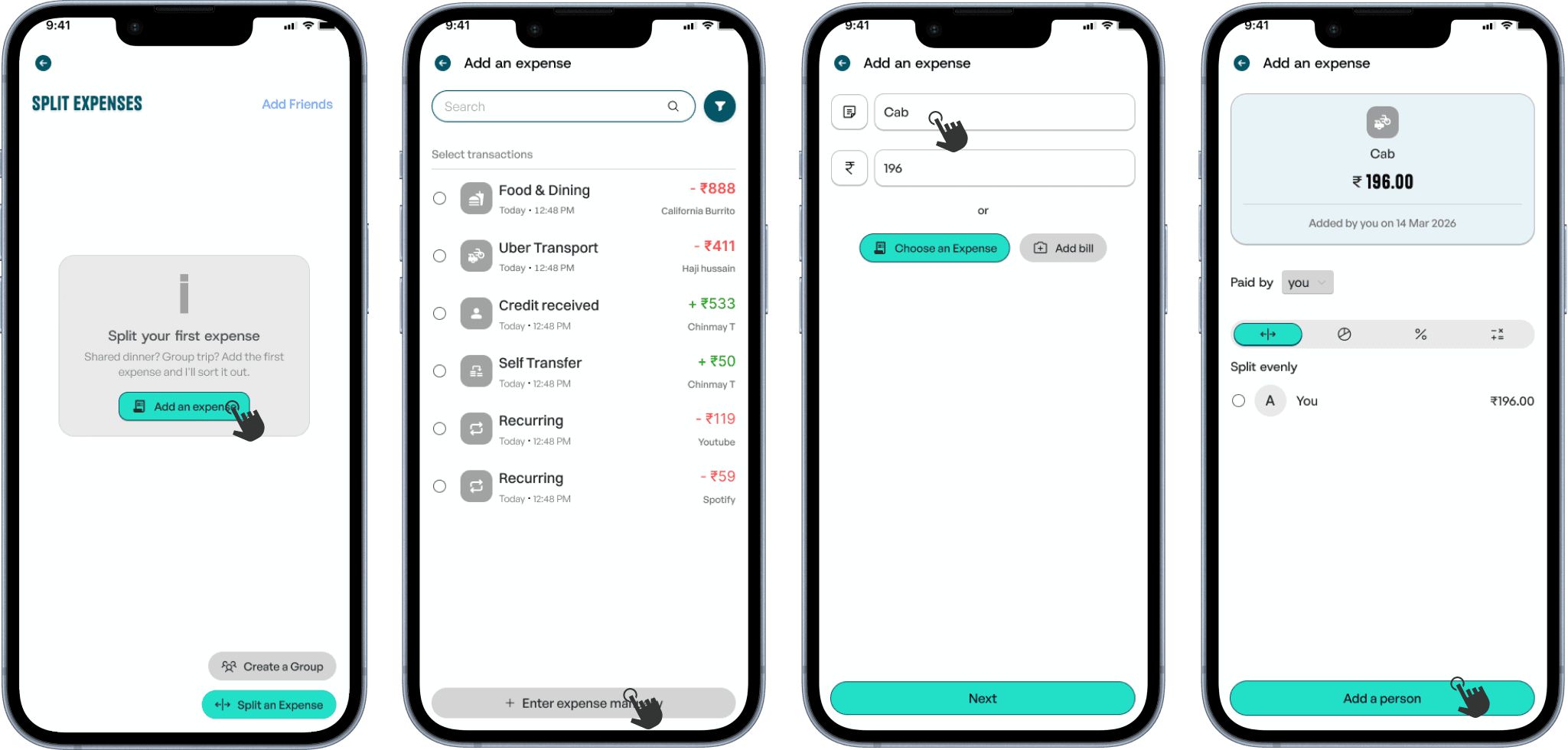

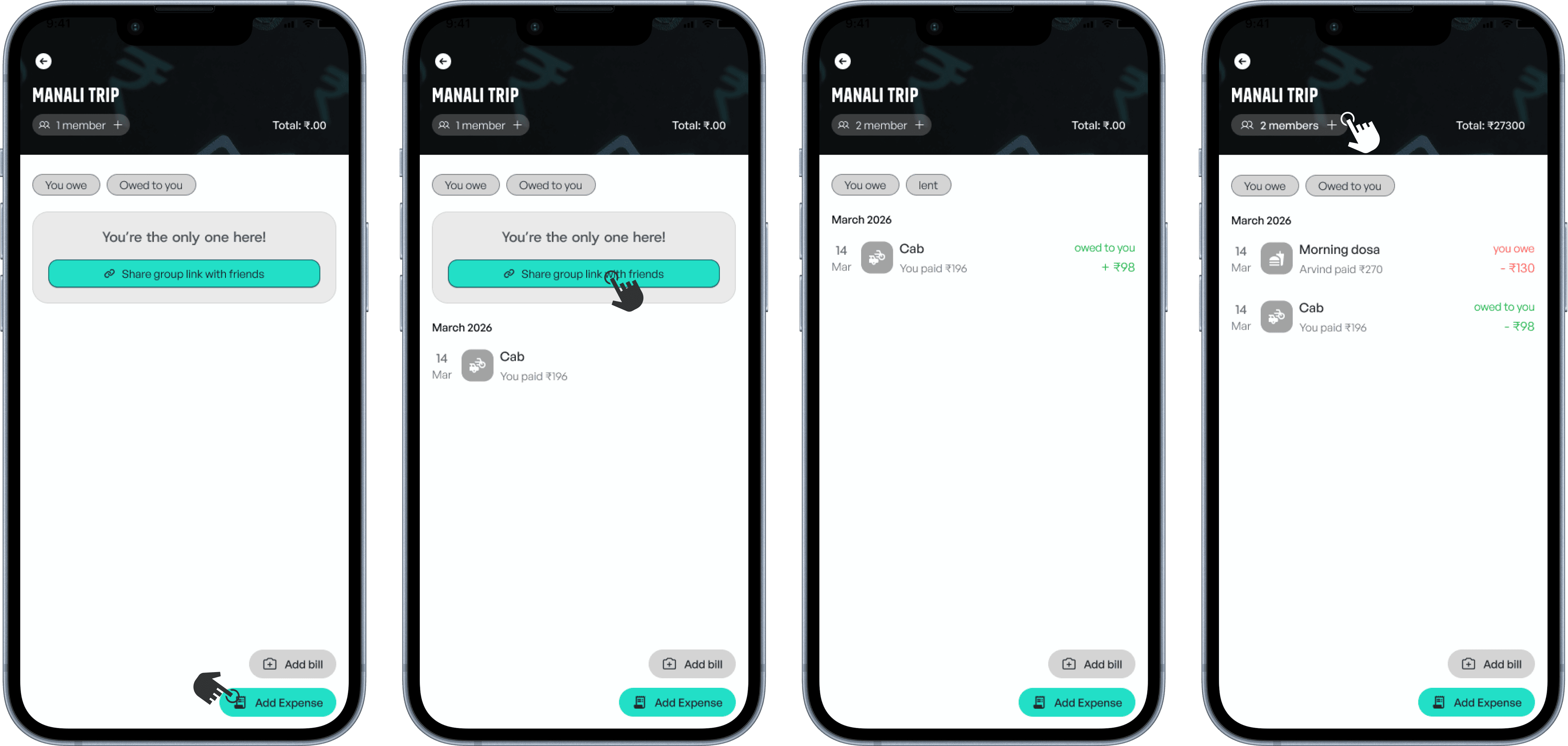

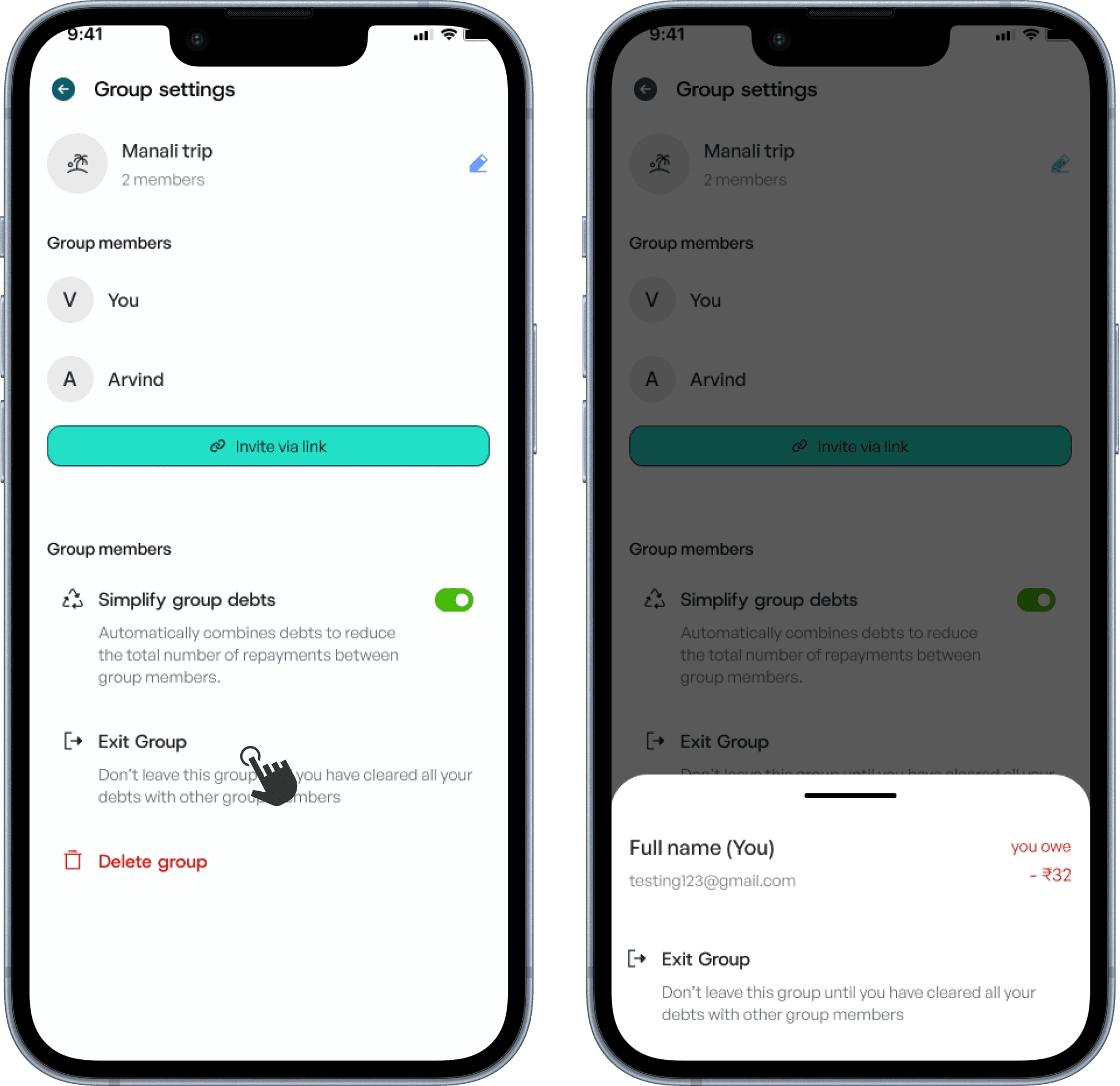

Payment split groups - Exploration

Add friends, split transactions, and automatically create groups. Or build groups from scratch to track shared expenses with multiple people. View balances, settle debts, and manage who owes whom—all in one place.

Adding a Friend

Splitting an expense

Creating a group

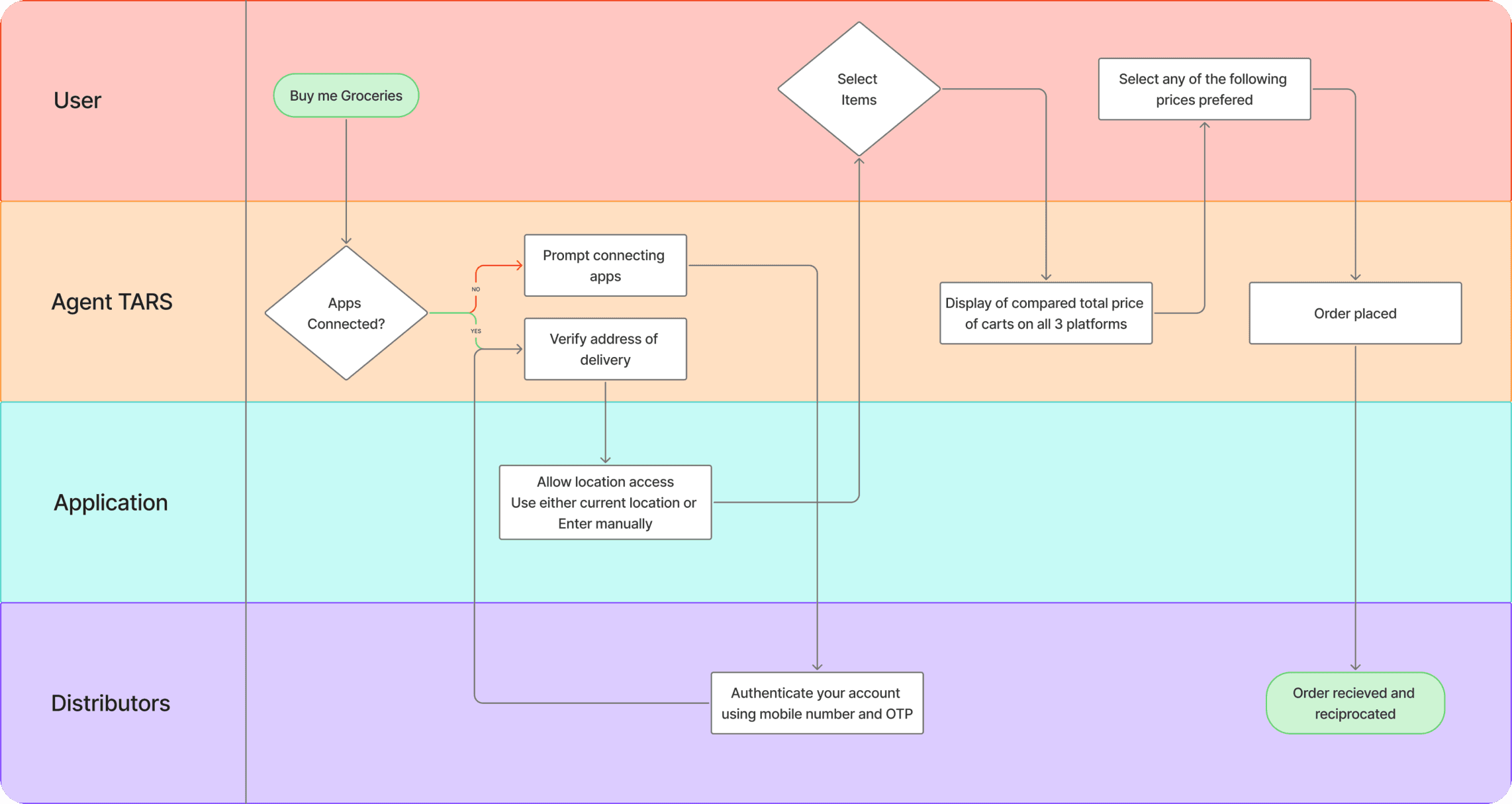

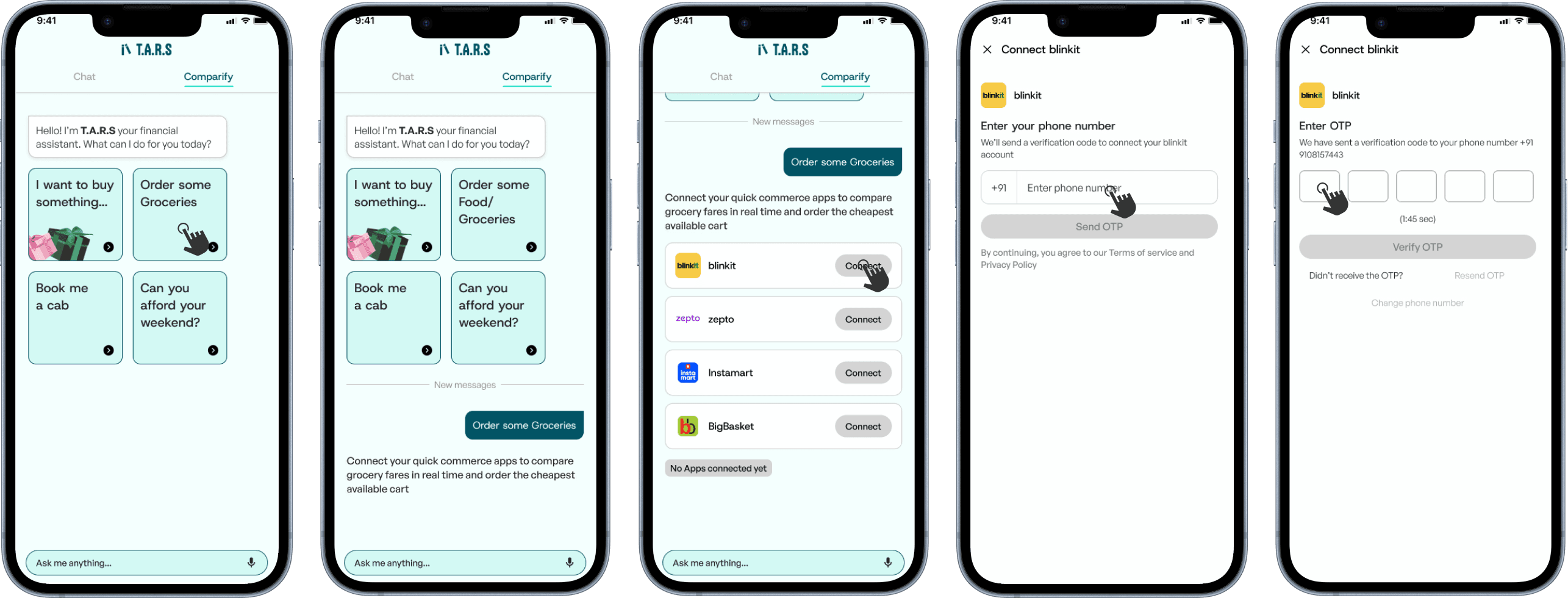

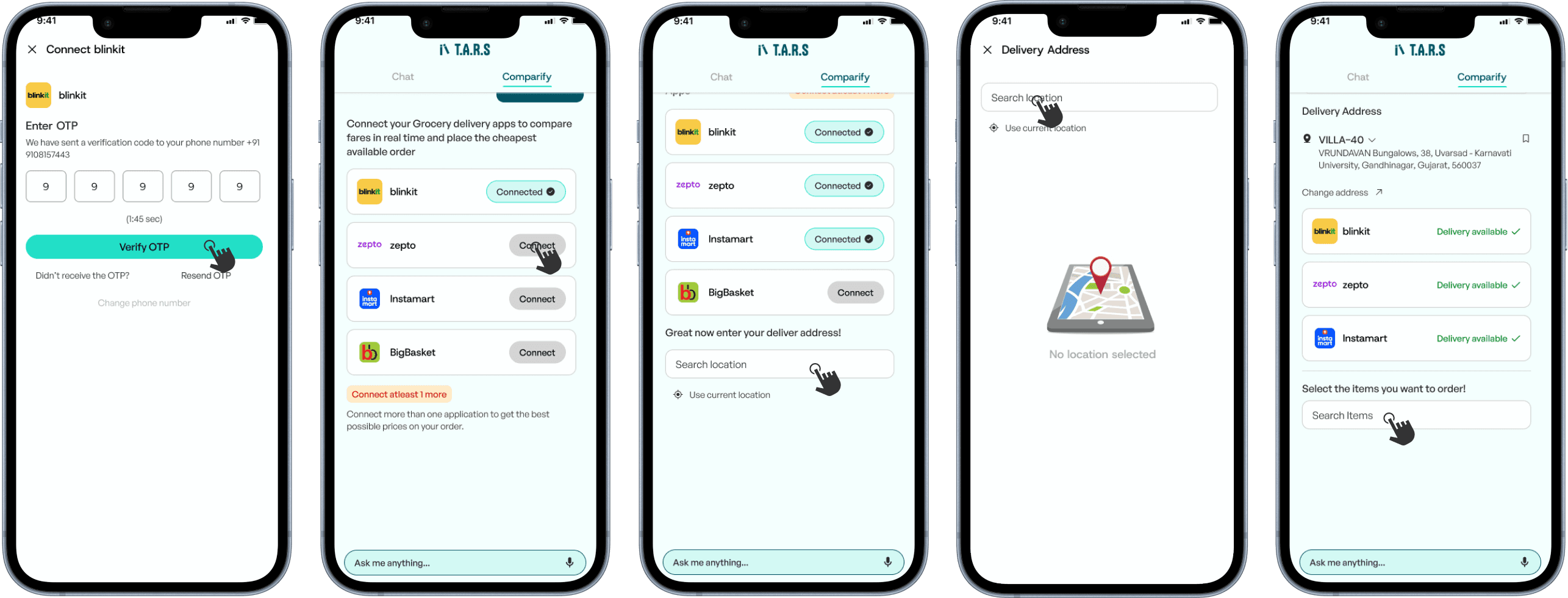

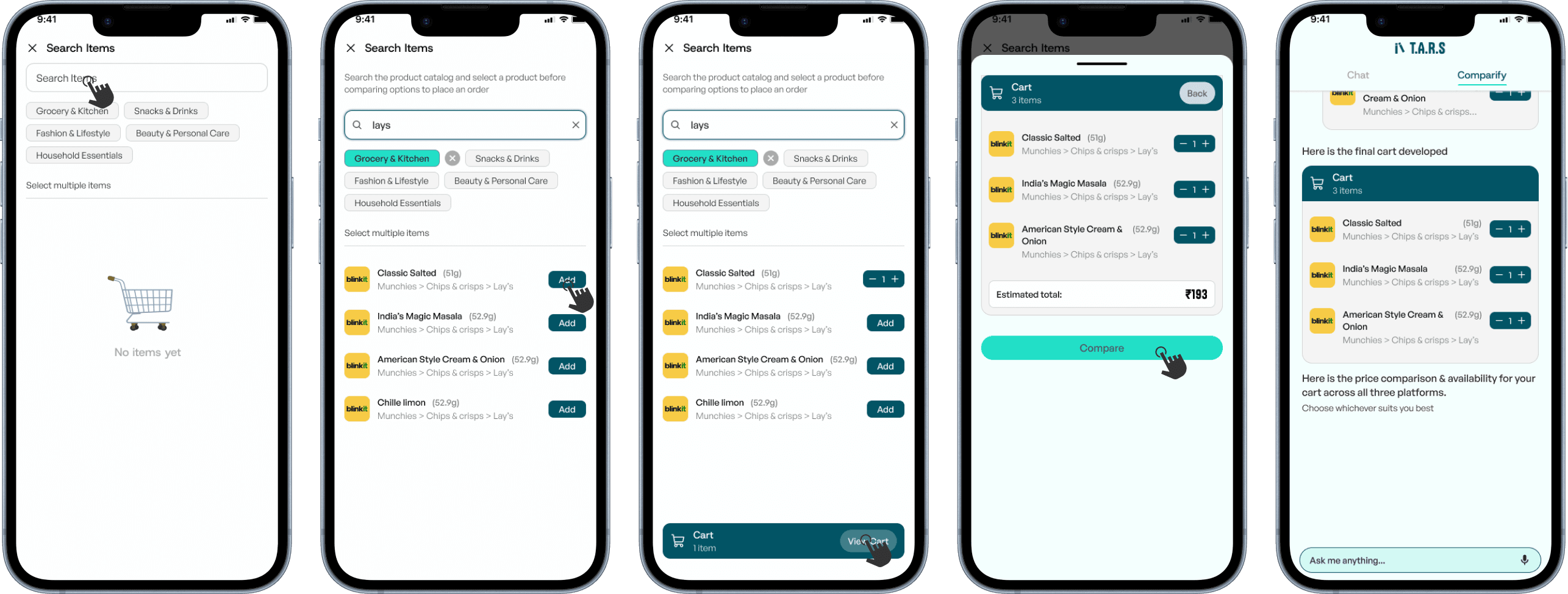

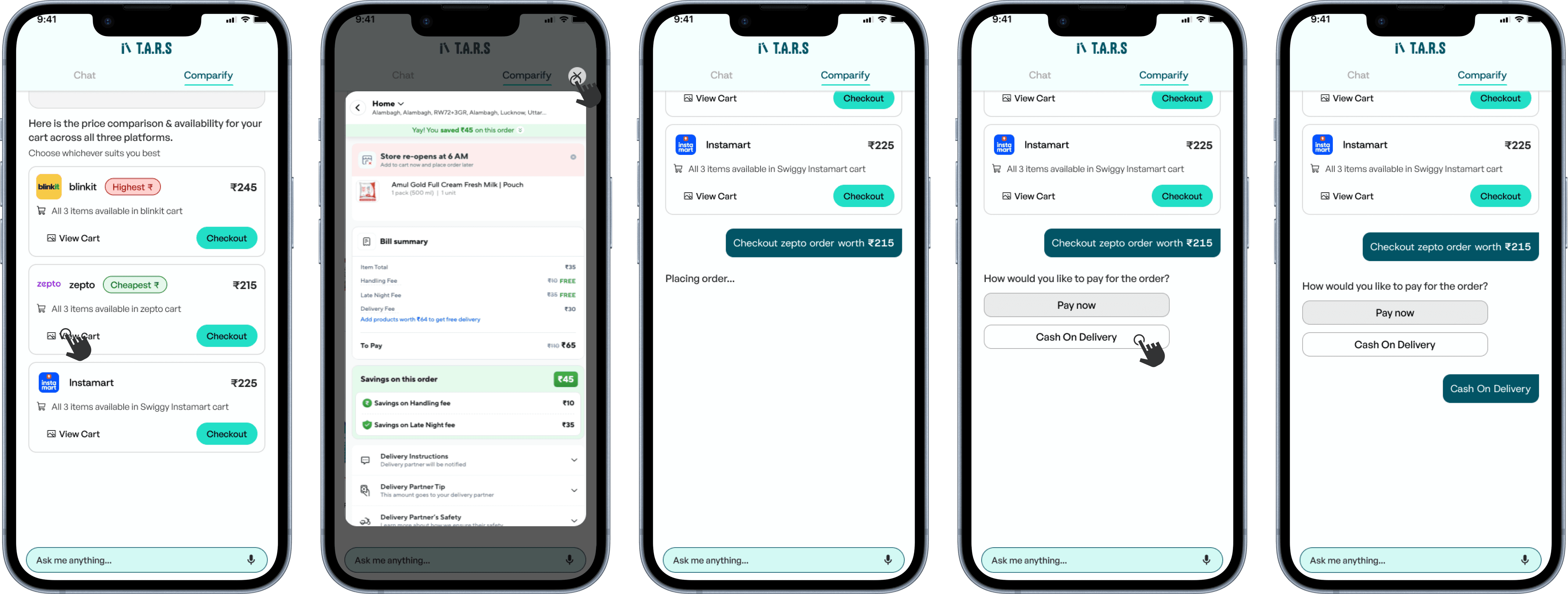

Agentic T.A.R.S - Exploration

Agentic T.A.R.S

Key takeaways

Things Left Unexplored

Design System Exploration

Exploring “Pot” for Passive Growth

Gamifying Budgeting Experiences